As India strides towards its goal of becoming a $5 trillion economy, the Union Budget for 2026-27, presented against a backdrop of robust post-pandemic recovery and global economic recalibration, has unveiled a taxation framework that seeks to balance fiscal consolidation with sustained growth. The budget, built on the pillars of simplification, innovation, and inclusivity, marks a decisive shift in the nation’s revenue architecture, aiming to stimulate investment, ease compliance, and ensure a more equitable distribution of the tax burden.

Consolidating the Direct Tax Vision: Stability and Carrots for Growth

A hallmark of the 2026 Budget is its reinforcement of stability in direct taxes. Having undergone significant reforms in preceding years, including reduced corporate tax rates and a streamlined personal income tax regime with optional slabs, the focus now is on consolidation and targeted incentives.

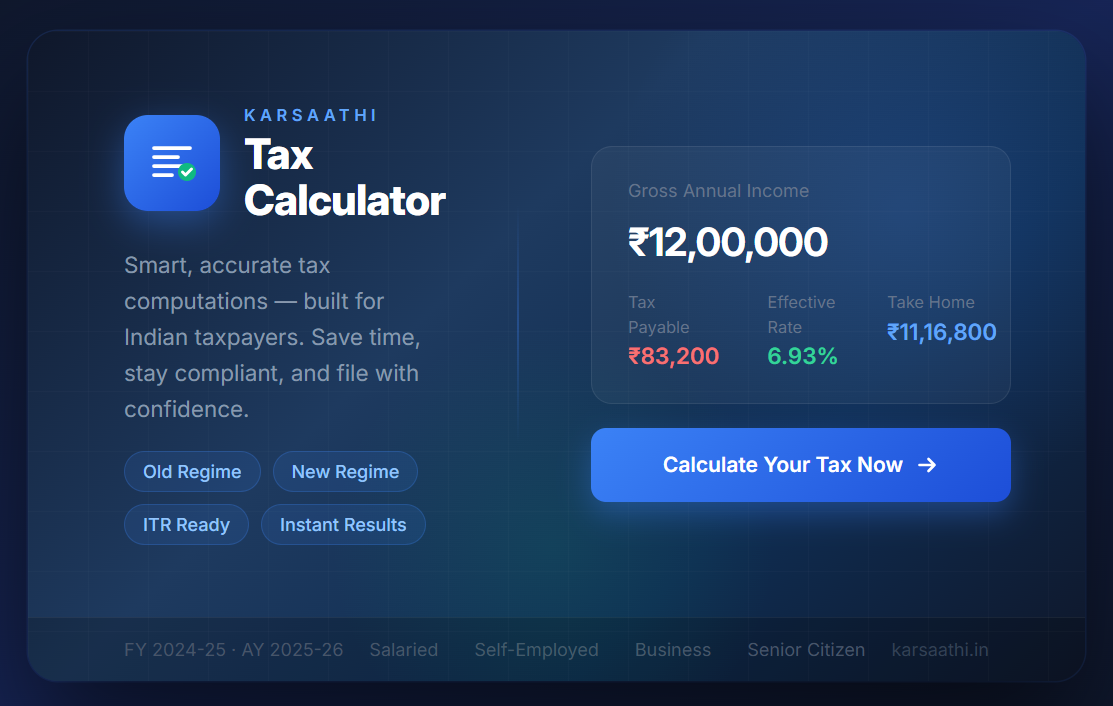

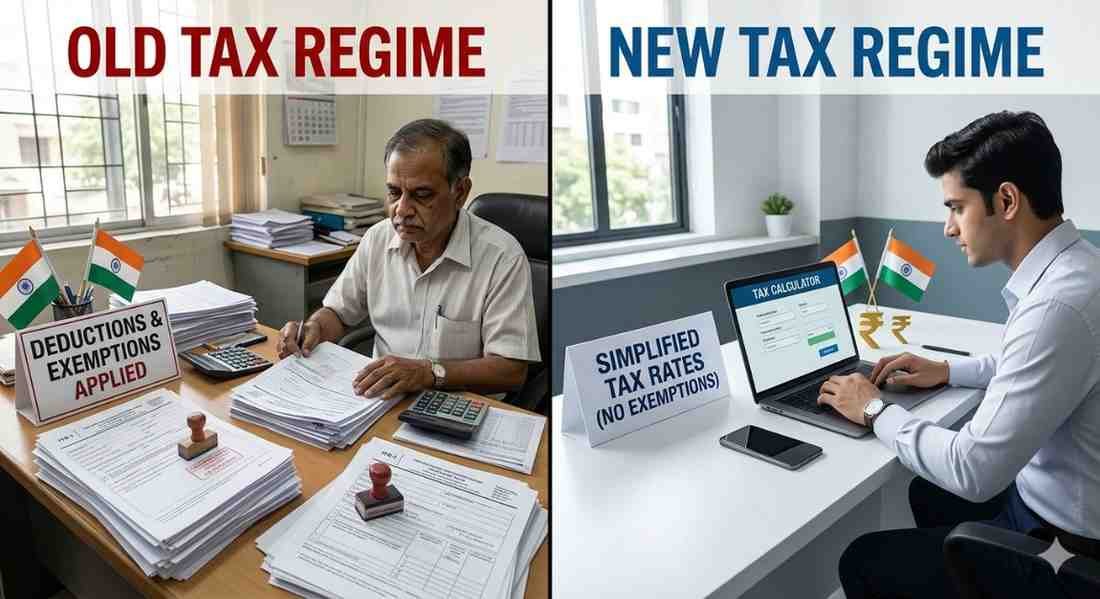

For Individual Taxpayers, the budget has made the new, simplified tax regime the default option, while retaining the old regime for those who wish to continue with deductions. The tax slabs have been marginally adjusted for inflation, providing modest relief to the middle class and boosting disposable income. Notably, the budget has significantly enhanced the limits for deductions on investments in National Pension System (NPS) and health insurance, recognizing the need to bolster social security and healthcare preparedness. A new, much-discussed introduction is the “Green Investment Deduction”—a Section 80C-like benefit for investments in approved renewable energy projects and ESG-focused mutual funds, aligning personal finance with national climate goals.

On the Corporate Front, the budget has doubled down on promoting ‘Make in India 2.0’ and research & development. A reduced tax rate of 15% for new manufacturing units setting up operations before March 2027 has been extended to include advanced technology sectors like semiconductors, green hydrogen, and aerospace. To fuel innovation, a weighted deduction of 200% on in-house R&D expenditure has been reintroduced, specifically for technologies aimed at import substitution and decarbonization.

Indirect Taxes: GST Refinement and Sin Tax Recalibration

The Goods and Services Tax (GST), now in a mature stage, has seen further refinement. The budget announced a roadmap to rationalize the remaining multiple tax slabs into a three-tier structure (a merit rate, a standard rate, and a demerit rate) over the next two years. Immediate steps include moving several common-use items from the 18% to the 12% bracket and clarifying ambiguous classifications to reduce litigation.

A significant move is the integration of petroleum products (excluding ATF) into the GST ambit, a long-pending reform. While this may lead to a temporary spike in fuel prices, it is expected to create a seamless credit chain for logistics and transportation sectors, ultimately reducing costs and inflation in the medium term.

“Sin taxes” on tobacco, sugary beverages, and alcohol have been steeply hiked, following a dual policy of generating revenue and discouraging consumption for public health reasons. A new “Plastic Packaging Cess” has been introduced on non-recyclable packaging, earmarked for funding circular economy initiatives.

The Digital & Green Economy: New Frontiers for Taxation

Budget 2026 firmly addresses the realities of the new economy. Provisions for the taxation of Virtual Digital Assets (VDAs or cryptocurrencies) have been tightened. The controversial TDS on VDA transfers remains, but the budget introduces a clear distinction between investment assets (like Bitcoin) and utility tokens, with differential tax treatment. Furthermore, a framework for reporting and taxation of income generated from the sale of AI models and large datasets has been introduced, ensuring India captures value from its booming digital innovation sector.

The green transition is a major revenue and policy theme. A “Carbon Border Adjustment Mechanism” (CBAM)-style import levy on carbon-intensive goods like steel and cement has been proposed, protecting domestic industry from cheaper, non-compliant imports and incentivizing greener production methods.

Compliance and Enforcement: Ease with Teeth

True to its promise of “Ease of Doing Business 3.0,” the budget announced the full implementation of the “NextGen Income Tax Portal” with AI-driven pre-filled returns, including capital gains from all financial institutions. The faceless assessment scheme is being strengthened with a dedicated appellate unit.

However, this ease is coupled with sharper enforcement tools. The tax net is being widened through tighter integration of data from GSTN, banks, financial institutions, and high-value transaction registers. A new, stricter General Anti-Avoidance Rule (GAAR) compliance window has been announced for legacy cases, signaling a no-nonsense approach towards aggressive tax planning.

The Road Ahead: Balancing Act for Amrit Kaal

The Union Budget 2026’s tax proposals represent a nuanced balancing act. By offering growth-oriented incentives, simplifying GST, and boldly embracing the taxation of new-age economies, it aims to fuel the investment cycle. The enhanced focus on green and social security deductions seeks to align taxpayer behavior with broader national objectives.

The success of this blueprint, however, hinges on seamless implementation and continuous dialogue with stakeholders. As India navigates the ‘Amrit Kaal’—its journey towards a developed nation by 2047—the tax system envisaged in Budget 2026 is clearly designed not just as a revenue collection tool, but as a strategic instrument for shaping a more productive, equitable, and sustainable economic future. The message is clear: contribute to India’s growth story, and the tax system will work as an enabler, not a hurdle.

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of

experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises.

Extpertise internal audit of Private enterprises. Audit planning through business understanding,

preliminary analytical procedures, determining materiality levels, and preparation of audit

program and pre-audit checklist . He is well conversant with the auditing standards issued by

ICAI. .