Mortgage Rates(Calculator) Today in the United States

Average Mortgage Rates:

- 30-Year Fixed-Rate Mortgage: Approximately 6.81%, slightly down from previous weeks but still near recent highs. New York Post+2AP News+2Credible+2

- 15-Year Fixed-Rate Mortgage: Around 5.94%, offering a lower rate for those opting for shorter loan terms. Bankrate+2AP News+2Mortgage Research Center+2

- 5/1 Adjustable-Rate Mortgage (ARM): Approximately 5.83%, providing initial lower rates that adjust after five years. Bankrate

- 30-Year Fixed Jumbo Mortgage: Rates are close to 6.72%, catering to loans exceeding conforming loan limits. Bankrate

As of May 1, 2025, specific mortgage rates from individual U.S. banks are not publicly disclosed. However, based on available data, the average 30-year fixed mortgage rates are as follows:

| Lender | 30-Year Fixed Rate | APR |

|---|---|---|

| Bank of America | 6.625% | 6.928% |

| Wells Fargo | 6.625% | 6.780% |

| U.S. Bank | 6.625% | 6.750% |

| Chase Bank | 6.625% | 6.750% |

| Citibank | 6.625% | 6.750% |

| PNC Bank | 6.625% | 6.750% |

| TD Bank | 6.625% | 6.750% |

| Truist Bank | 6.625% | 6.750% |

| Capital One | 6.625% | 6.750% |

| DHI Mortgage | 5.33% | N/A |

Current Landscape: Are Mortgage Rates Going Down or Up?

As of early 2025, mortgage rates remain a hot topic. Following a steep climb during 2022 and 2023, driven largely by the Federal Reserve’s aggressive rate hikes aimed at taming inflation, rates reached levels not seen in over a decade. While inflation has begun to cool, the question persists: Will mortgage rates go down?

Why Mortgage Rates Are Going Up (or Not Falling Quickly)

Mortgage rates are influenced by a variety of economic factors, but most directly by the federal funds rate, inflation expectations, and bond yields—particularly the 10-year Treasury yield. Here's a closer look at why mortgage rates may still be high:

Federal Reserve Policy: The Fed has maintained a cautious stance in reducing interest rates. While they've paused hikes, they haven’t aggressively cut rates yet due to persistent inflation in some sectors.

Sticky Inflation: Even as overall inflation cools, certain areas such as housing costs and insurance premiums are rising, preventing rapid monetary policy loosening.

Global Uncertainty: Geopolitical tensions and market volatility cause investors to demand higher yields for long-term lending, including mortgage-backed securities, thereby pushing mortgage rates up.

In short, the lingering effects of inflation and the Fed’s reluctance to shift too quickly are primary answers to why mortgage rates going up or remaining elevated.

Will Mortgage Rates Go Down in 2025?

Market analysts are split. Some forecast modest decreases in the second half of 2025 as inflation trends downward and the Fed gains confidence to lower rates. Others believe rates will stay relatively flat until stronger economic data supports a cut.

What to Watch:

CPI and PCE inflation data

Federal Reserve statements and dot plots

Bond market trends

If inflation remains on track and no new economic shocks occur, there’s potential for mortgage interest rates to gradually decrease. However, sudden global or domestic instability could reverse that trend.

What Mortgage Can I Afford?

When planning to purchase a home, understanding what mortgage you can afford is crucial. This depends on a combination of your income, debt, down payment, and the mortgage interest rate. Here’s how to evaluate your affordability:

1. Income and Debt-to-Income Ratio (DTI)

Lenders typically prefer a DTI ratio below 43%. That means your monthly debt payments—including the potential mortgage—shouldn’t exceed 43% of your gross monthly income.

2. Down Payment

The larger the down payment, the smaller your loan and monthly payment. Conventional loans often require at least 5%, while FHA loans may allow as low as 3.5%.

3. Credit Score and Rate Offered

Your credit score directly impacts the mortgage interest rate you're offered. A higher score can significantly reduce your monthly payment over time.

Using a Mortgage Amortization Calculator

To make an informed decision, use a mortgage amortization calculator. This tool helps you break down your monthly payments over the life of the loan, showing how much goes to interest vs. principal.

What Can You Learn from It?

Monthly payment amount

Total interest paid over time

How early payments impact your loan balance

Effects of making extra payments

Try adjusting inputs like interest rate or loan term (e.g., 15 vs. 30 years) to see how your payments change. This insight is crucial when rates are volatile, as a slight shift can change your affordability threshold.

The Role of a Mortgage Broker

A mortgage broker acts as an intermediary between borrowers and lenders, helping you find the best loan options. With today’s complex market, their expertise is often invaluable.

Why Use a Broker in 2025?

Rate Shopping: They have access to multiple lenders and can help secure competitive rates.

Loan Product Advice: Whether you’re looking for an ARM (adjustable-rate mortgage) or a conventional fixed-rate loan, brokers guide you to the right choice.

Streamlining Paperwork: Brokers handle much of the application and approval process, saving time and reducing errors.

In uncertain times, using a broker can help you better navigate fluctuating mortgage interest rates and lending standards.

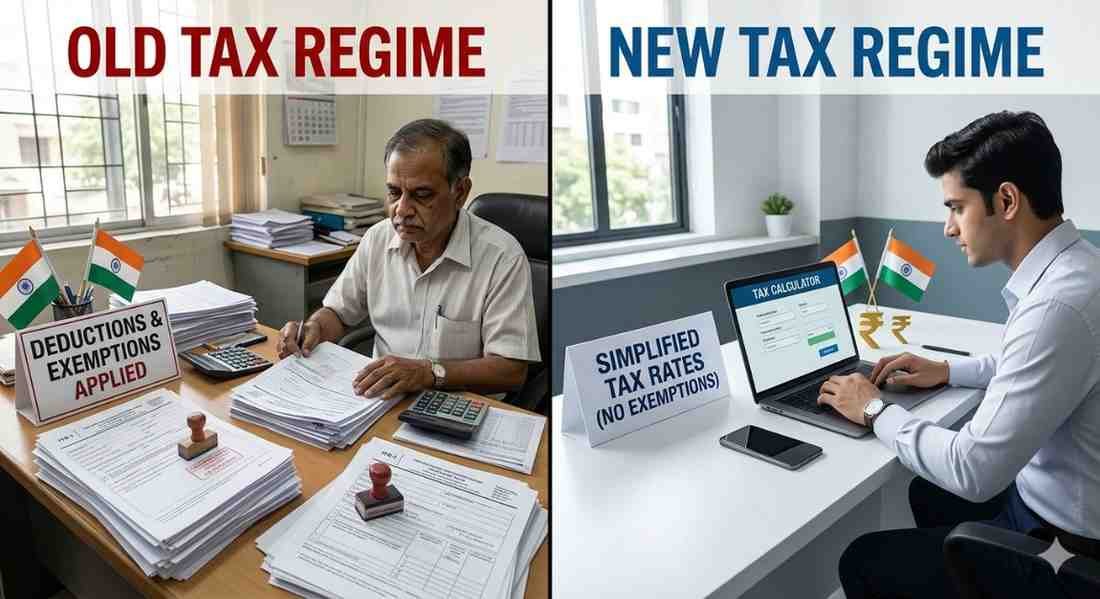

Types of Mortgage Products in Today’s Market

Understanding your mortgage options is also key to affordability. Here are the most common products in 2025:

Fixed-Rate Mortgages

Still the most popular option, offering consistent monthly payments for 15 or 30 years. Beneficial in a high-rate environment if you expect rates to remain elevated.

Adjustable-Rate Mortgages (ARMs)

ARMs offer lower initial rates that adjust after a set period. They’re gaining popularity in 2025 as buyers bet on rates falling in the next few years.

Government-Backed Loans (FHA, VA, USDA)

Designed for first-time buyers, veterans, or those purchasing in rural areas, these loans often offer lower down payments and favorable terms.

Strategies for Buyers in a High-Rate Environment

Even if mortgage rates are not going down significantly yet, you can still find ways to make homeownership affordable.

1. Buy Down the Rate

Sellers or lenders may offer to "buy down" your rate via discount points, reducing your interest rate for a cost paid upfront.

2. Refinance Later

Consider locking in a home purchase now, with the plan to refinance when (or if) rates drop in the future.

3. Expand Location Flexibility

Explore areas where home prices are lower, helping offset the impact of high rates.

4. Use a Mortgage Broker for Options

Leverage their network to find niche products or lenders offering promotional rates.

Mortgage Broker & Mortgage Rates – FAQ

1. What is a mortgage broker?

A mortgage broker is a licensed professional who acts as a middleman between borrowers and lenders. They help you find the best mortgage product for your financial situation by comparing loan options from various lenders.

2. Why should I use a mortgage broker instead of going directly to a bank?

Mortgage brokers offer access to a wide range of lenders and loan products, which can help you secure a more competitive interest rate or better loan terms. They also handle much of the paperwork and negotiation on your behalf.

3. Do mortgage brokers charge a fee?

In most cases, mortgage brokers are paid by the lender, not the borrower. However, depending on the loan or situation, there may be fees involved. Always ask your broker to clearly outline any fees upfront.

4. How do mortgage rates work?

Mortgage rates are the interest rates charged on a home loan. They can be fixed (stay the same over the term) or variable (change with the market). The rate you’re offered depends on several factors including your credit score, down payment, loan type, and current market conditions.

5. What’s the difference between fixed and variable rates?

Fixed-rate mortgages lock in your interest rate for the full term of the loan.

Variable (or adjustable) rate mortgages start with a lower rate that can fluctuate over time, based on market conditions.

6. How is my mortgage rate determined?

Lenders consider several factors:

Credit score and history

Employment and income stability

Loan amount and down payment

Loan term (e.g., 15-year vs. 30-year)

Debt-to-income ratio

Market interest rates

7. Can I get pre-approved for a mortgage?

Yes! Pre-approval helps you understand what you can afford and shows sellers you’re a serious buyer. A mortgage broker can assist with the pre-approval process by submitting your application to potential lenders.

8. How long does mortgage approval take?

It varies depending on the complexity of your application and the lender, but it typically takes between 1–3 weeks from application to approval.

9. Can a mortgage broker help with refinancing?

Absolutely. Mortgage brokers can help you refinance your current mortgage by comparing new loan options to lower your rate, adjust your term, or access home equity.

10. How do I get started with a mortgage broker?

You can begin by contacting a licensed mortgage broker, providing your financial details, and discussing your homeownership goals. They’ll guide you through the options and next steps.

Author : Uttam Bisht

30 April, 2025 | 05:51 AM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

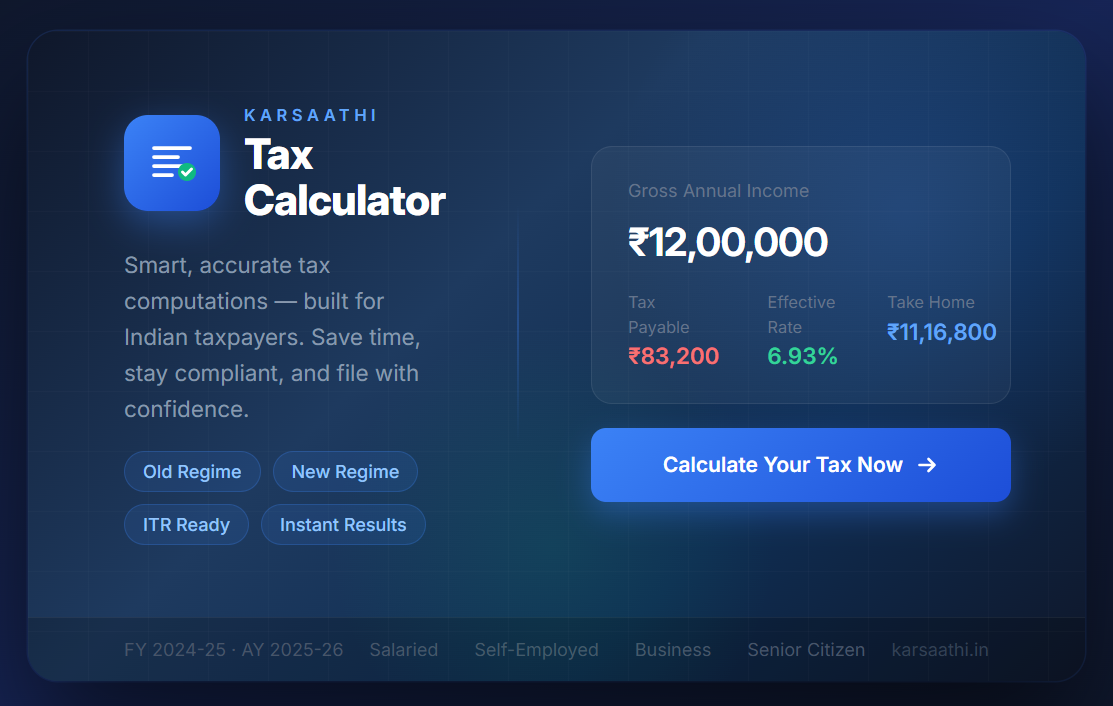

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

26 April, 2025 | 10:23 PM

How Bank's are scamming you - Fixed vs Reducing Rate

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM