How Banks Are Scamming You – Fixed vs Reducing Rate Explained

When it comes to borrowing money, most of us are focused on the big questions: “What’s the interest rate?”, “What’s the EMI?”, “Can I afford this loan?” But lurking behind those shiny advertisements and “low interest” offers is a quiet little trick that banks and lending institutions use to squeeze out more money from your pocket: the difference between fixed rate and reducing balance rate.

It might sound like a small technical detail, but this difference can cost you thousands (or even lakhs) over the life of your loan. Let's break it down and see how this game works.

What Are Fixed and Reducing Rates?

At the most basic level, both fixed and reducing rates are ways of calculating how much interest you owe on a loan. But they differ in how the interest is calculated over time.

1. Fixed Interest Rate

In a fixed interest loan, the interest is calculated on the entire principal amount for the full tenure of the loan, regardless of how much you’ve already repaid.

Let’s say you take a loan of ₹10 lakhs at 10% fixed interest for 5 years. Every year, you pay 10% on ₹10 lakhs — even though your loan balance is decreasing over time.

That’s like paying rent for a house you’ve already moved out of.

2. Reducing (or Diminishing) Interest Rate

In a reducing interest loan, the interest is calculated only on the outstanding loan amount, which means as you repay the principal, your interest goes down.

Using the same example: ₹10 lakhs loan at 10% reducing interest for 5 years means your interest is calculated on the balance remaining after each EMI payment.

This method is far more logical and fair — but here’s the catch — banks rarely offer both side-by-side, and they use this difference to confuse or mislead borrowers.

How Banks Use This To Their Advantage

The main scam is this:

Banks advertise fixed rate interest because it sounds lower than it actually is.

If a bank offers you a loan at 10% fixed rate, it may look cheaper than a 12% reducing rate at first glance — but in reality, the effective interest paid is much higher with the fixed rate loan.

Here’s why:

Because in a fixed rate loan you keep paying interest on the full principal, you end up paying significantly more over time.

Let’s do some quick math to show the difference:

A Simple Example: ₹50 Lakh Loan Over 20 Years

| Type of Interest | Interest Rate | Total Interest Paid |

|---|---|---|

| Fixed | 10% | ₹10000000 (approx) |

| Reducing | 10% | ₹6580240 (approx) |

That’s a difference of ₹34.19 lakh — on the same amount and same rate.

In fact, to compare apples to apples:

A 10% fixed interest rate is roughly equal to 18–19% reducing rate!

Conversely, a 10% reducing rate is like a 5.5–6% fixed rate.

This massive gap is rarely communicated transparently.

EMI Confusion – Another Trap

Another sneaky tactic? Showing lower EMIs.

Let’s say two banks are offering you a loan:

Bank A: ₹10 lakh at 10% fixed rate

Bank B: ₹10 lakh at 10% reducing rate

Bank A will show you a lower EMI, making it seem more affordable. But since the EMI is calculated over interest on the full principal, you’ll pay way more over time.

Most borrowers don’t do the math — and banks know this.

The “Flat Rate” Scam

In some personal loans, especially from NBFCs (non-banking financial companies), you’ll hear the term flat rate. This is just another name for fixed rate.

They’ll advertise something like:

“Get a personal loan at just 12% flat interest!”

Sounds amazing, right?

But that 12% flat rate is equivalent to 21–22% reducing rate. That’s loan shark territory, and yet it’s totally legal and often hidden behind flashy marketing.

Why This Continues to Happen

Let’s be real — banks are not in the business of doing charity. Their goal is to make money. And the average borrower doesn’t have the time, tools, or understanding to navigate the complexity of loan structures.

This allows banks and financial institutions to use fine print, ambiguous terminology, and misleading advertisements to sell you a worse deal than you think you’re getting.

The regulators haven’t cracked down on this hard enough either. While RBI and SEBI have guidelines around transparency, many institutions get away with creative phrasing and selective disclosure.

How You Can Protect Yourself

Here’s how to avoid getting played:

1. Always Ask for Reducing Rate Equivalent

If someone quotes a fixed or flat rate, ask:

“What is the effective reducing balance rate equivalent of this offer?”

If they hesitate or try to dodge, that’s a red flag.

2. Use an Online EMI Calculator

Plug in both reducing and flat rate values to see the true EMI and total interest payable. Plenty of websites offer these tools for free.

3. Get the Full Amortization Schedule

Demand a detailed payment schedule — this shows how much of each EMI goes toward principal vs interest.

4. Don’t Be Fooled by Low EMIs

A lower EMI might just mean you’re paying more in the long run.

5. Read the Fine Print

Yes, it’s tedious. But often the fixed vs reducing rate trick is hidden in footnotes, or buried under jargon.

Conclusion: Don’t Let the Glossy Ads Fool You

In the world of finance, language is a weapon, and banks use terms like “flat rate”, “fixed interest”, or “low EMI” to confuse and entice you. Understanding the difference between fixed and reducing rates could literally save you lakhs of rupees.

So the next time someone offers you a “low interest loan”, dig deeper. Ask questions. Do the math. Because behind that friendly banking smile might just be a clever trap waiting to spring.

Fixed vs Reducing Rate — FAQ

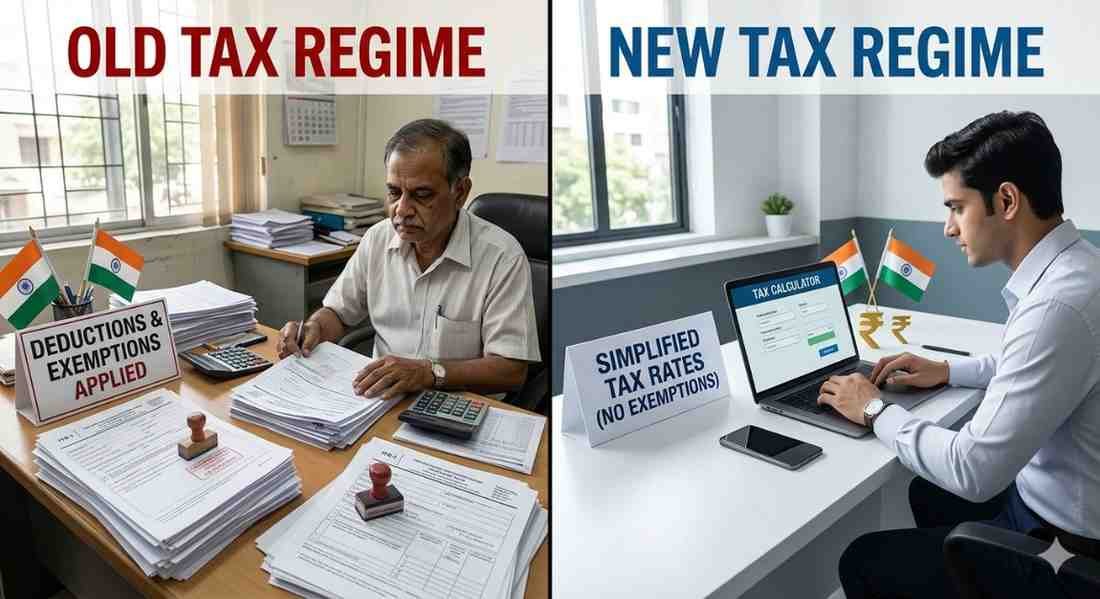

1. What is a Fixed Rate?

A Fixed Rate means the interest rate stays constant throughout the loan or deposit tenure. Your monthly payments remain the same, making it easier to budget and plan.

2. What is a Reducing Rate?

A Reducing Rate (also called Diminishing or Declining Balance Rate) means the interest is charged only on the outstanding loan amount. As you repay, the interest amount decreases over time.

3. How do repayments differ between Fixed and Reducing Rates?

Fixed Rate: You pay the same EMI (Equated Monthly Installment) each month.

Reducing Rate: Your EMI can either stay the same with more principal paid over time, or reduce depending on the structure.

4. Which one is cheaper: Fixed or Reducing Rate?

Typically, Reducing Rates work out cheaper overall because interest is calculated on a lower principal amount each month. However, it's important to compare effective interest rates carefully.

5. Why would someone choose a Fixed Rate?

Fixed rates offer stability and predictability — perfect for those who prefer a consistent monthly budget without worrying about market fluctuations.

6. When is a Reducing Rate better?

Reducing rates are better if you plan to prepay your loan early or want to save on overall interest costs over time.

7. Are Fixed Rates truly "fixed" forever?

Not always. Some loans offer a fixed rate only for an initial period (like 2–5 years) and then switch to a floating rate. Always check the loan agreement carefully!

8. Which rate is better during a rising interest rate environment?

A Fixed Rate is generally safer if you expect market interest rates to go up, because your rate (and EMI) won’t change.

9. How can I compare Fixed and Reducing Rates?

Look at the Annual Percentage Rate (APR) or Effective Interest Rate for an apples-to-apples comparison. Fixed rates may seem lower at first glance but could be higher when adjusted for reducing calculations.

10. What should I consider before choosing?

Your financial stability

Future interest rate trends

Flexibility for prepayment

Total cost of the loan

Your comfort with risk

Other Bogs:

Author : Uttam Bisht

26 April, 2025 | 10:23 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

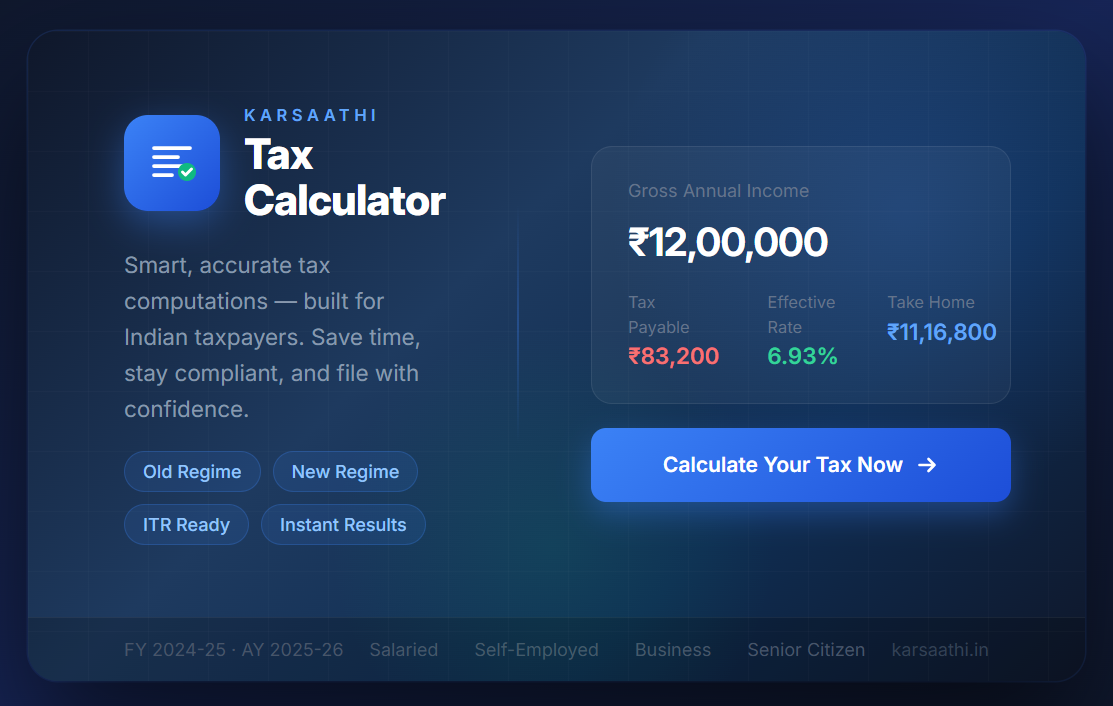

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM