NPS Process in India:

The National Pension System (NPS) is a voluntary, long-term retirement savings scheme initiated by the Government of India. It aims to provide financial security to individuals during their post-retirement years. Launched in 2004 for government employees and later extended to all Indian citizens in 2009, NPS has gained popularity as a secure and flexible investment option.

Retirement planning is a crucial aspect of financial security, yet it's often overlooked until it’s too late. One essential component in securing a stable retirement is the National Pension Scheme (NPS). Introduced by the government, the NPS aims to provide financial stability and a secure future for its subscribers. This blog post delves into the specifics of the National Pension Scheme, highlighting its benefits, eligibility criteria, investment choices, and how to maximize its advantages for a comfortable retirement.

What is NPS?

The National Pension System is a market-linked, defined contribution pension scheme managed by the Pension Fund Regulatory and Development Authority (PFRDA). It allows individuals to systematically save for their retirement and provides a stable income post-retirement.

Types of NPS Accounts:

NPS offers two types of accounts:

Tier-I Account:

This is the primary retirement account and has restrictions on withdrawals.

A minimum annual contribution of ₹1,000 is required to keep the account active.

Withdrawals before retirement are subject to specific rules.

Tier-II Account:

This is a voluntary savings account with flexible withdrawal options.

Unlike the Tier-I account, there are no restrictions on withdrawals.

There is no tax benefit on contributions to this account (except for government employees).

Eligibility for NPS

Any Indian citizen (resident or non-resident) aged 18-70 years can open an NPS account.

The applicant must comply with Know Your Customer (KYC) norms.

NPS is available to salaried employees, self-employed individuals, and even corporate employees.

How to Open an NPS Account?

Online Method (eNPS Portal)

Visit the eNPS website (https://enps.nsdl.com/ or https://enps.karvy.com/).

Select the option to register for NPS as an individual.

Choose between Aadhaar-based or PAN-based registration.

Fill in the required details such as name, date of birth, address, and contact information.

Upload the scanned copies of your Aadhaar, PAN, and canceled cheque.

Select the preferred Pension Fund Manager (PFM) from the available options.

Choose the Investment Option (Auto or Active mode) and allocate funds among asset classes.

Make the initial contribution (minimum ₹500 for Tier-I and ₹1,000 for Tier-II).

After completing the payment, you will receive a Permanent Retirement Account Number (PRAN).

Download and sign the PRAN application form, and send it to the Central Recordkeeping Agency (CRA).

Offline Method

Visit the nearest Point of Presence (PoP) (banks, financial institutions, post offices).

Collect the NPS application form.

Fill in personal and nominee details and attach self-attested KYC documents.

Submit the form along with an initial contribution (minimum ₹500 for Tier-I and ₹1,000 for Tier-II).

You will receive the PRAN kit by post, which includes your PRAN card, password, and subscriber details.

NPS Contribution Guidelines:

The minimum contribution for Tier-I is ₹500 per transaction and ₹1,000 per annum.

The minimum contribution for Tier-II is ₹250 per transaction.

There is no maximum limit on the amount of contribution.

Subscribers can contribute through net banking, debit/credit card, UPI, or direct deposit.

Contributions are invested in different asset classes (Equity, Corporate Bonds, Government Bonds, and Alternative Investments) based on the chosen allocation.

Withdrawal and Exit Rules in NPS:

Exit Before Retirement (Before 60 Years)

Allowed after 10 years of investment.

Up to 20% of the corpus can be withdrawn as a lump sum.

The remaining 80% must be used to purchase an annuity.

Withdrawal at Retirement (After 60 Years)

60% of the accumulated corpus can be withdrawn as a lump sum (tax-free).

40% must be used to buy an annuity to receive a regular pension.

Partial Withdrawals

Allowed after 3 years for specific purposes such as higher education, marriage of children, medical emergencies, or home purchase.

A maximum of 25% of the contribution can be withdrawn.

Only three withdrawals are allowed during the entire tenure.

Tax Benefits of NPS:

For Salaried Individuals

Under Section 80CCD(1):

Contributions up to 10% of salary (Basic + DA) are eligible for a deduction (up to ₹1.5 lakh per annum).

Under Section 80CCD(1B):

An additional deduction of ₹50,000 for NPS contributions.

Under Section 80CCD(2):

Employer contributions up to 10% of salary are tax-exempt (without any upper limit).

For Self-Employed Individuals

Eligible for a deduction of up to 20% of gross income under Section 80CCD(1) (subject to ₹1.5 lakh limit).

Additional ₹50,000 deduction under Section 80CCD(1B).

Taxation on Withdrawal

60% of the corpus withdrawn at retirement is tax-free.

40% of the corpus, which is used to buy an annuity, is taxed as per the applicable income tax slab.

Any premature withdrawal is subject to taxation based on NPS rules.

Example of NPS under the Income Tax Act

Let’s assume Mr. Raj, a salaried individual, has the following details:

Basic Salary + DA: ₹10,00,000 per annum

NPS Contribution (self): ₹1,00,000

NPS Contribution (employer): ₹1,00,000

NPS Tax Deductions:

Under Section 80CCD(1): ₹1,00,000 (within 10% of salary, counted under the ₹1.5 lakh limit of Section 80C)

Under Section 80CCD(1B): Additional ₹50,000 deduction

Under Section 80CCD(2): Employer’s ₹1,00,000 contribution is fully deductible without any upper limit

Total Tax Deduction under NPS = ₹2,50,000, reducing his taxable income significantly.

National Pension System (NPS) - Frequently Asked Questions (FAQ)

1. What is the National Pension System (NPS)?

The National Pension System (NPS) is a government-sponsored retirement savings scheme open to employees from public, private, and unorganized sectors, including self-employed individuals. It is regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

2. Who can join the NPS?

Any Indian citizen (resident or non-resident) aged between 18 and 70 years can join the NPS. It is also open to employees of central and state governments, private sector employees, and self-employed individuals.

3. What are the types of NPS accounts?

NPS has two types of accounts:

Tier I Account: A mandatory retirement account with restrictions on withdrawal.

Tier II Account: A voluntary savings account with flexible withdrawals but requires an active Tier I account.

4. How can I open an NPS account?

You can open an NPS account through:

Online: Via eNPS portal using Aadhaar, PAN, or bank details.

Offline: By visiting a Point of Presence (PoP), such as banks or post offices.

5. What are the investment options in NPS?

NPS offers four asset classes for investment:

Equity (E)

Corporate Bonds (C)

Government Bonds (G)

Alternative Assets (A) (limited exposure) Subscribers can choose between Auto Choice (age-based allocation) or Active Choice (self-selection of asset allocation).

6. How much should I contribute to NPS?

Tier I: Minimum contribution at the time of account opening is ₹500, with an annual minimum of ₹1,000.

Tier II: Minimum contribution at the time of account opening is ₹250, with no annual minimum requirement.

7. What are the tax benefits of NPS?

Under Section 80CCD(1): Employee contributions up to 10% of salary (20% for self-employed) are tax-deductible within the ₹1.5 lakh limit under Section 80C.

Under Section 80CCD(1B): Additional tax deduction of up to ₹50,000.

Under Section 80CCD(2): Employer’s contribution (up to 10% of salary) is deductible without the ₹1.5 lakh cap.

8. When can I withdraw from NPS?

At Retirement (60 years): 60% of the corpus can be withdrawn tax-free, and 40% must be used to purchase an annuity.

Early Withdrawal: Allowed after 3 years for specific purposes like education, marriage, home purchase, or medical treatment, with a limit of 25% of the contributions.

Exit Before 60: 20% can be withdrawn, and 80% must be used for an annuity purchase.

9. Can I change my fund manager or investment choice?

Yes, NPS allows subscribers to change their Pension Fund Manager (PFM) and switch between Auto and Active investment choices.

10. How can I check my NPS balance?

You can check your NPS balance online by logging into the Central Recordkeeping Agency (CRA) portal using your Permanent Retirement Account Number (PRAN).

11. What happens in case of the subscriber’s death?

Before 60 years: The entire corpus is paid to the nominee/legal heir.

After 60 years: The nominee can withdraw the corpus or continue with the annuity option.

12. How can I exit from NPS?

At Retirement (60 years): Withdraw up to 60% as a lump sum and invest 40% in an annuity.

Before Retirement (before 60 years): Withdraw 20% and invest 80% in an annuity.

Death: The entire corpus is given to the nominee/legal heir.

13. Is NPS better than other retirement plans like EPF or PPF?

NPS has higher equity exposure and offers market-linked returns, while EPF and PPF provide fixed interest rates. The choice depends on risk tolerance and investment goals.

14. Can an NRI invest in NPS?

Yes, Non-Resident Indians (NRIs) can invest in NPS. However, withdrawals are subject to FEMA regulations.

15. How do I contact NPS customer service?

You can contact NPS through the PFRDA website, CRA service providers like NSDL and Karvy, or your Point of Presence (PoP).

Author : Uttam Bisht

14 February, 2024 | 11:30 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

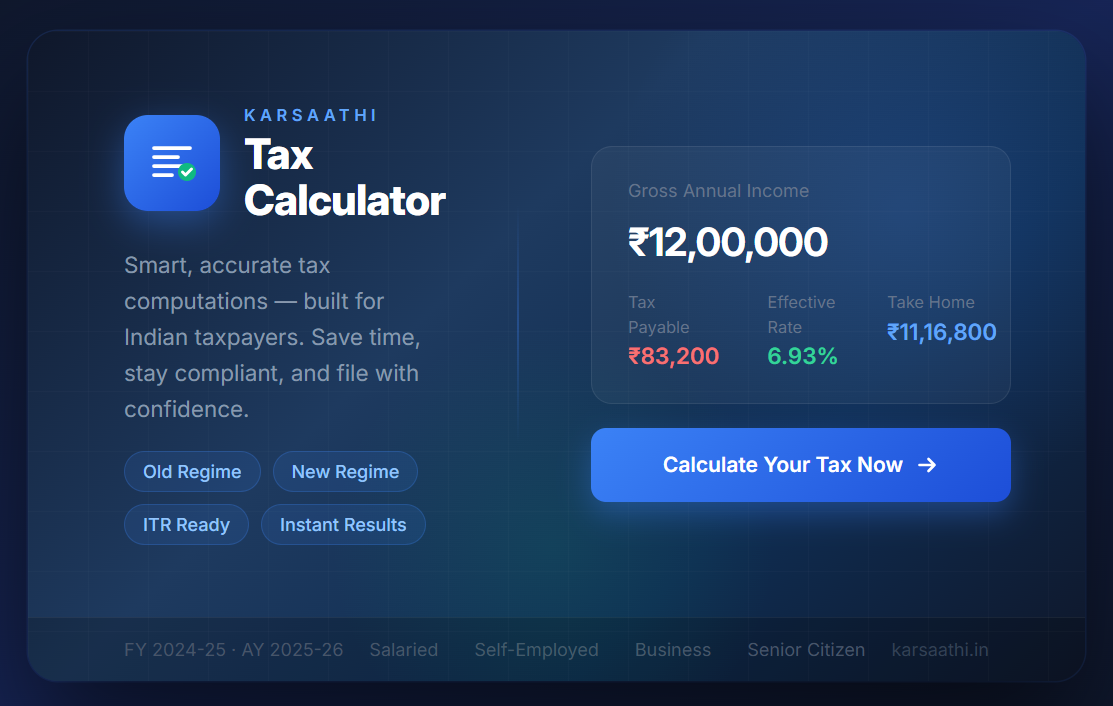

Karsaathi Income Tax Calculator

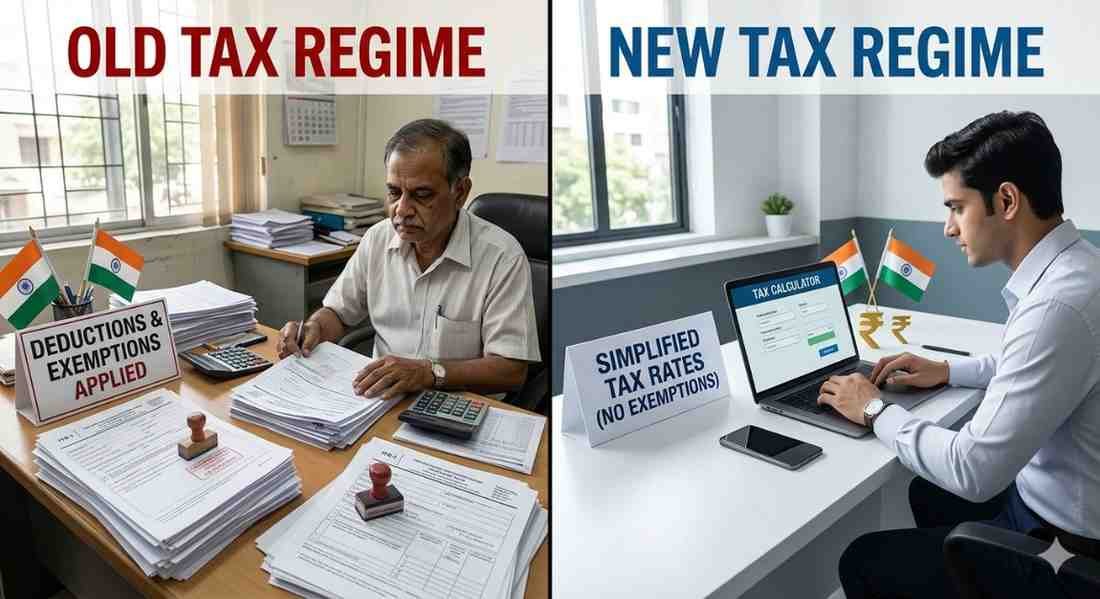

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM