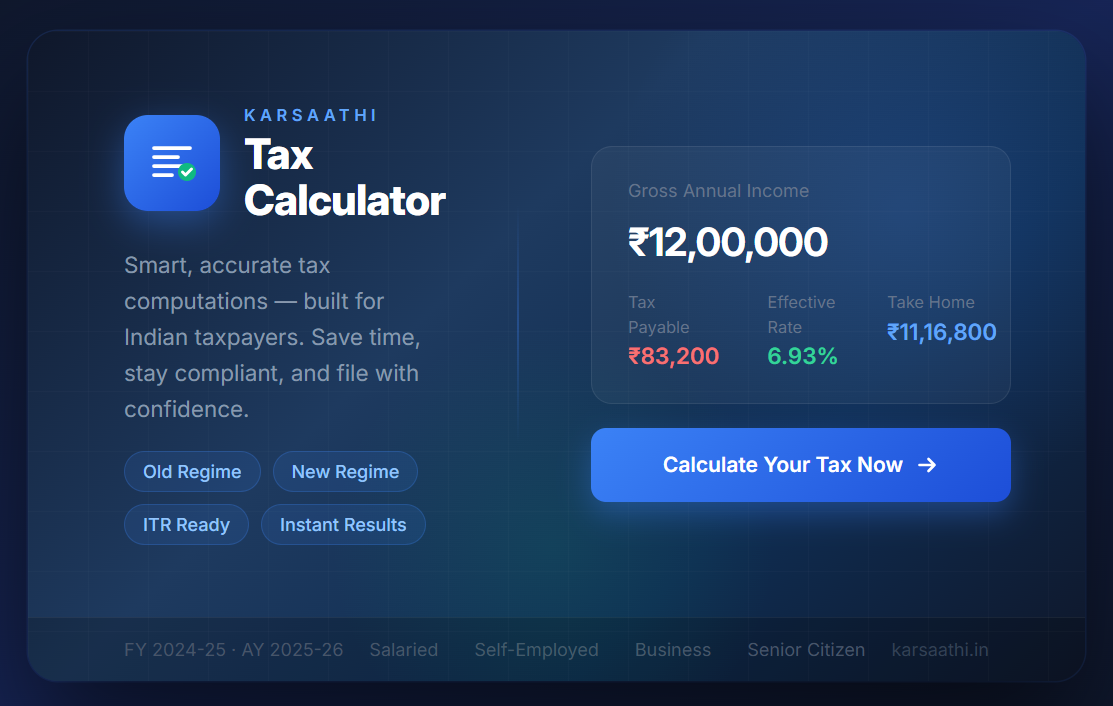

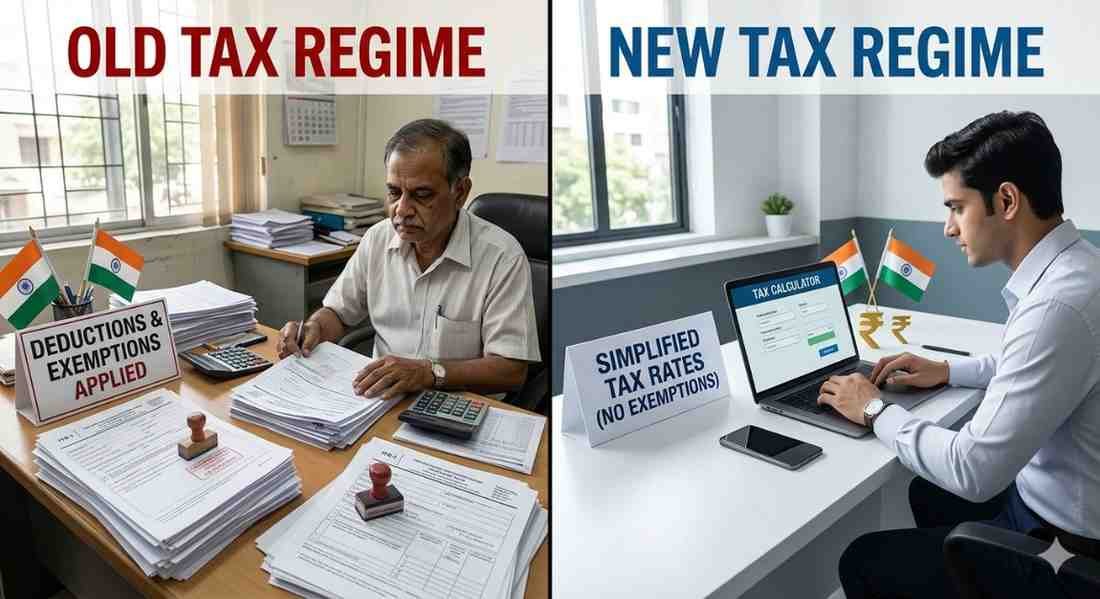

New Tax Regime VS Old Tax Regime 2023?

NRIs can avail the new tax regime in India, which increases the basic exemption to Rs. 3,00,000. However, they cannot claim the rebate on full tax for income up to Rs. 7,00,000, which is only available to residents.

Here At KarSaathi We Provide You Best Taxation Services:

Tax Consultants in Delhi

ITR Filling Service

Income Tax Consultancy

Accounting services in south west Delhi

What is new tax regime and old tax regime?

Finance Minister Nirmala Sitharaman announced the new tax regime in Budget 2020 giving taxpayers the option to choose between it and the existing tax structure when they file their taxes. While your income will be taxed at lower rates as per the new tax slab, there is a catch. You will no longer be able to utilize the deductions under the Income Tax Act as earlier, to lower your tax liability any further.

Is new tax regime beneficial?

Which tax regime is better old or new for salaried employees?

If you do not invest in tax-saving instruments:

In her budget speech, the finance minister explicitly stated that a person with an annual income of Rs 15 lakh not availing any deductions as per the proposed tax structure will have to pay only Rs 1.56 lakh as tax as opposed to Rs 2.73 lakhs in the old regime. New tax rules allow for greater tax savings for income above 15 lakhs in this case, as illustrated below.

| Old Tax Structure | Tax Calculation | New Tax Structure | Tax Calculation |

| 5%(2.5L-5L) | 12,500 | 5% (3L-6L) | 15000 |

| 20%(5L-10L) | 10,0000 | 10% (6L-9L) | 30000 |

| 30%(10L&>) | 150000 | 15% (9L-12L) | 45000 |

| Total (1+2+3) | 262000 | 20% (12L-15L) | 60000 |

| Cess (4%) | 10,500 | Cess (4%) | 6000 (Total Tax =150000*4%) |

| Income Tax | 273000 | Income Tax | 156000 |

If you avail deductions worth 2.5 lakh or more:

If your annual income is between 15 lakhs to 20 lakhs and you claim tax deductions worth 2.5 lakh, you have the option to choose between either of the two regimes since the tax payable will be more or less the same. However, if you are focused on tax saving for income above 15 lakhs and the amount of exemption in tax sought by you is more than 2.5 lakhs, it is prudent to stick to the old method of tax computation. Let us understand this by looking at tax computation by both methods for a person drawing a yearly salary of Rs 20 lakhs.

How to Save Tax for Income above Rs. 15 Lakhs?

An additional tax benefit is available for contributions of up to Rs 50,000 to the Scheme as per 80CCD(1B) provisions taking the total to Rs 2 lakh.

1. Reduce Your Taxable Income by Up To Rs 1.5 Lakhs (Section 80C, 80CCC)

SECTION 80C DEDUCTION SAVE TAX UP TO 1.5 LAKH

- Life insurance premium

- Equity Linked Savings Scheme (ELSS MUTUAL FUND)

- Employee Provident Fund (EPF)

- Annuity/ Pension Schemes

- Principal payment on home loans

- Tuition fees for children

- Contribution to PPF Account

- Sukanya Sam Riddhi Account

- NSC (National Saving Certificate)

- Fixed Deposit (Tax Savings)

- Post office time deposits

- National Pension Scheme

- stamp duty, registration fee, and other expenses for transfer of such house property to the assessee.

2. Additional Reduction of Up To Rs 50,000 for NPS Investors (Section 80CCD)

a) The maximum deduction available on self-contribution to the NPS Tier-1 account is limited to:

10% of annual income for salaried investors

20% of annual income for self-employed investors

b) You can contribute an additional amount for a deduction of up to Rs 50,000 a year

3. Reduce Your Taxable Income by Up To Rs 75,000 (Section 80D)

a) Health insurance for yourself and your family

Reduces your taxable income by up to Rs 25,000 if you are below 60

Includes preventive health check-up expenses of up to Rs 5000

Cover your children below 25 years of age under the same plan

b) Health Insurance for your parents

Reduce your taxable income by up to Rs 50,000 more if parents are 60 or above

(Rs 25,000 for below 60)

You can claim medical expenses as well for senior citizen parents

Include preventive health check-up expenses of up to Rs 5000

4. Reduce Your Taxable Income by Up To Rs 2 lakhs (Section 24)

Tax Calculation for Annual Income of 20 Lakhs :

Old Regime vs New Regime

| Details | Tax Calculation (Old) | Tax Calculation (New) |

| Salary Drawn | 20,00000 | 20,00000 |

| Standard Deduction | 50,000 | NIL |

Income under Salary Deduction u/s 24(Home Loan Interest) | 1950000 200000 | 2000000 NIL |

Chapter VI A Exemptions80D 80CCD NPS | 150000 50000 | Nil |

Taxable Income Less: Exempt Total Income | 1525000 (250000) 1275000 | 20,00000 (350000) 1650000 |

| Income Tax | 270000 | 285000 |

| 4% Cess | 10800 | 11400 |

| Tax Payable | 280800 | 296400 |

How can I save tax if I earn 15 lakh?

From the above table, you can easily see that you can claim various deductions on your salary income. Now, you can save tax if you earn a salary of Rs 15 lakhs, here’s a table that will show you how to save tax for a salary above 15 lakhs:

| Deductions to be claimed | Available Deduction (₹) |

| Standard Deduction | 50,000 |

| Investment’s u/s 80 C | 150,000 |

| Medical insurance premium u/s 80 D | 25,000 |

| Additional Deduction on NPS* | 50,000 |

| Home loan interest | 200,000 |

| Total | 475,000 |

From the above, you can see that if your income is Rs 15 LPA, you can claim various deductions from taxable income up to Rs 4.75 lakhs.

Note: You can avail of the deductions and exemption only if you opt for the old tax regime. These deductions and exemptions are not available in the new tax regime.

How much tax do I pay on 15 lakhs?

Here is the table showing how much tax does have to pay on Rs 15 lakhs income if you opt for old and new tax regimes:

Note: The deductions and exemptions are not available in the new tax regime.

| Category | Old Tax Regime (₹) | New Tax Regime (₹) |

| Income | 15,00,000 | 15,00,000 |

| Deductions | 4,75,000 | 150000 |

Taxable incomeLess: Exempt Total Income | 10,25,000 775000 | 350000 1150000 |

| Income tax | 120000 | 140000 |

| Add:Cess 4% | 4800 | 5600 |

| Net Tax liability | 124800 | 145600 |

The best way to save tax for a salary above 15 lakhs is to opt for the old tax regime and claim all the available deductions and exemptions on tax-saving investments.

Demerits of New Tax Regime:

Deductions and exemptions not allowed against business income:

- Additional depreciation under section 32

- Investment allowance under section 32AD

- Sector-specific business deductions under sections 33AB and 33ABA

- Expenditure on scientific research under section 35

- Capital expenditure under section 35AD

- Exemption under section 10AA for SEZ units

NOTE: In the case of a business income, an individual or HUF cannot claim set-off of the brought forward business loss or unabsorbed depreciation.

The deductions are not available under the new regime to the extent they relate to deductions/exemptions withdrawn.

Author : Uttam Bisht

14 February, 2024 | 11:19 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM