House Rent deduction | HRA exemption rule

House Rent deduction | HRA exemption rule

The following are some considerations about HRA tax exemptions:

1. You cannot claim the HRA tax exemption if you are paying rent to your spouse.

2. You can use the HRA exemption from income tax even if you have a home loan.

3. If you live with your parents, you can apply for a House Rent Allowance by paying your rent to them and receiving a receipt.

4. If your annual rent is more than one lakh rupees, you must submit the PAN information of your landlord.

5. A 30% TDS (Tax Deducted at Source) must be subtracted from the rent before it can be paid in the case of an NRI landlord.

Who is eligible for HRA?

Can non salaried person claim HRA?

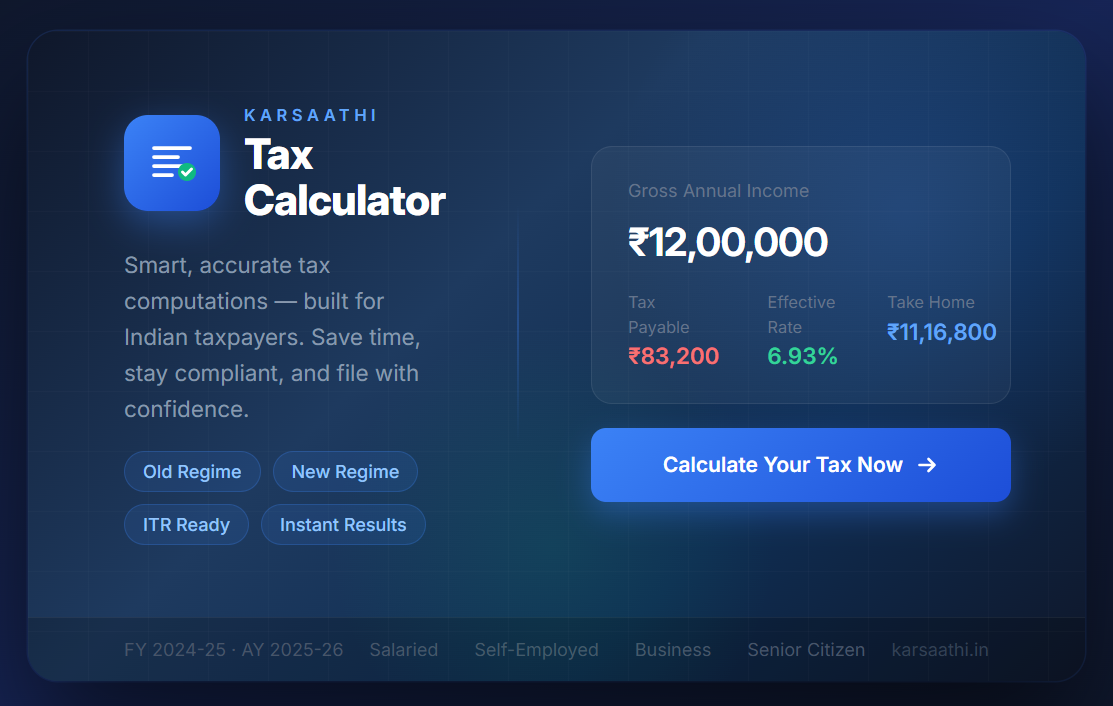

USE HRA CALCULATOR FOR COMPLEX TAX CALCULATION

What are the 3 conditions for HRA exemption?/HRA Kaise Milta Hai

The tax exemption for HRA is the minimum of:

i) Actual HRA received

ii) 50% of salary if living in metro cities, or 40% for non-metro cities; and

iii) Excess of rent paid annually over 10% of annual salary for calculation purpose, the salary considered is ‘basic salary’.

In case ‘Dearness Allowance (DA)’ (if it forms a part of retirement benefits) and ‘commission received based on sales turnover’ is applicable, they too are added to compute the minimum HRA exemption available. The tax benefit is available to the person only for the period in which the rented house is occupied.

Example of HRA calculation :HRA Kaise Milta Hai

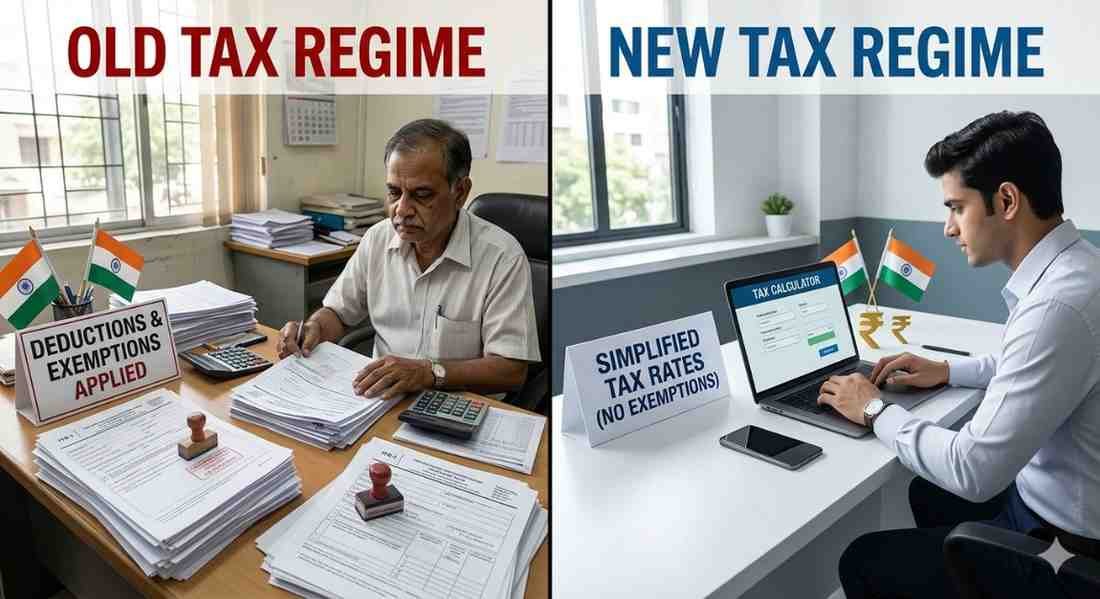

Let’s say an individual, with a monthly basic salary of Rs 55,000, receives HRA of Rs 15000 and pays Rs 9800 rent for accommodation in a metro city. The tax rate applicable to the individual is 20 percent on his income under the old tax regime.

To avail of HRA benefit, the least of the following amount (yearly) is exempted, and the rest is taxable: i) Actual HRA received = Rs 180,000 (15000 x 12) ii) 50% of salary (metro city) = Rs 330,000 (50% of Rs (55,000 x 12 = 660,000)) iii) Excess of rent paid annually over 10% of annual salary = Rs 51,600 (Rs 117600* – (10% of Rs 660000)) *9800X12 = 117600

It shows that of Rs 180,000 received as HRA, Rs 51,600 gets tax exemption and only the balance of Rs 128400 gets added to the employee’s income.

Documents For Claiming HRA :

HRA exemptions can be availed only on submission of rent receipts or the rent agreement with the house owner. An employee must report the PAN of the ‘landlord’ to the employer if the rent paid is more than Rs 1,00,000 annually to avail of the tax benefit.

Paying rent to family members:

The rented premises must not be owned by the person claiming the tax exemption. So if you stay with your parents and pay rent to them then you can claim that for tax exemption under HRA. However, you cannot pay rent to your spouse. As, in the view of the relationship, you are supposed to take the accommodation together.

Even if you are renting the house from your parents, make sure you have documentary evidence as proof that financial transactions regarding your tenancy take place between you and your parent. So keep a record of banking transactions and rent receipts because your claim can get rejected by the tax department if they are not convinced by the authenticity of the transactions. Previously, there has been an instance in which the HRA claim of a salaried taxpayer was rejected by the Mumbai income tax.

What Happens If I Don't Get an HRA?

You may still deduct the cost of renting a residential property under Section 80GG even if your employer does not provide an HRA. To qualify for this deduction, the following requirements must be met:

You either work for yourself or are paid. Throughout the year for which you are submitting your 80GG claim, you never got HRA. You, your spouse, your minor child, or the HUF of which you are a member do not own any residential property where you now dwell, perform official or employment-related activities, or conduct business or practise your profession.

You shouldn't claim the advantage if you own any residential property elsewhere besides the location indicated above.

Author : Uttam Bisht

14 February, 2024 | 11:18 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM