Which is the best retirement plan in india?

There is no one best retirement plan in India as the appropriate plan will depend on your individual financial goals, risk tolerance, and investment horizon. Some common retirement planning options in India include:

Public Provident Fund (PPF):

A PPF account is a long-term investment vehicle offered by the government of India. Contributions to a PPF account are eligible for tax deductions under Section 80C of the Income Tax Act, up to a maximum of INR 1.5 lakhs per financial year. In addition, the interest earned on a PPF account is tax-free.

Employee Provident Fund (EPF):

An EPF account is a retirement savings plan offered by most employers in India. Contributions to an EPF account are made by the employee and the employer, and the accumulated savings can be used to provide a regular income during retirement.

Pension Plans:

Pension plans are long-term investment products that are designed to provide a regular income during retirement. There are several types of pension plans available in India, including traditional pension plans, unit-linked pension plans, and National Pension System (NPS) plans.

Mutual Funds:

Mutual funds are investment vehicles that pool money from multiple investors and invest in a diversified portfolio of securities, such as stocks, bonds, and money market instruments. Mutual funds can be a good option for retirement planning as they offer the benefits of professional management and diversification.

Fixed Deposits:

Fixed deposits (FDs) are a type of savings instrument that offer a fixed rate of return over a predetermined period of time. FDs can be a good option for retirement planning as they offer a guaranteed rate of return and are generally considered to be a low-risk investment.

It is important to consider your individual financial goals and risk tolerance when choosing a best retirement plan. It is always a good idea to consult with a financial advisor before making any investment decisions.

What is a 401k How does it work?

A 401(k) is a type of retirement savings plan offered by many employers in the United States. It is named after the section of the Internal Revenue Code that governs its rules and regulations.

The way a 401(k) works is that an employee can choose to have a portion of their salary automatically withheld and deposited into their 401(k) account. These contributions are usually made before taxes are taken out of the employee's paycheck, which reduces the employee's taxable income for the year. Some employers also match a percentage of the employee's contributions, which is an additional benefit.

The money in the 401(k) account can then be invested in a variety of options, such as mutual funds, bonds, or stock. The investments grow tax-free until the employee reaches retirement age and starts to withdraw the money. At that point, the withdrawals are taxed as regular income.

One of the benefits of a 401(k) is that it allows employees to save for retirement in a tax-advantaged way. Additionally, many 401(k) plans offer a wide variety of investment options, allowing employees to diversify their portfolio.

There are some limits on the amount an employee can contribute to their 401(k) each year, as well as penalties for withdrawing the money before retirement age. It's important to understand the rules and regulations of your specific 401(k) plan and to speak with a financial advisor for personalized advice.

Which pension plan gives highest return?

What are the 3 types of retirement?

There are several different types of retirement plans, but some of the most common include:

- Traditional pension plans: These plans, also known as defined benefit plans, provide a set amount of income in retirement based on factors such as years of service and salary history. The employer is typically responsible for funding and managing the plan.

- 401(k) plans: These plans, also known as defined contribution plans, allow employees to contribute a portion of their salary to a retirement account that is typically invested in a variety of assets such as stocks and bonds. The employee is responsible for managing and investing the funds, and the employer may also contribute to the plan.

- Individual Retirement Accounts (IRAs): These are retirement savings plans that are available to individuals and are not employer-sponsored, they come in two types : Traditional IRA and Roth IRA. The traditional IRA contributions may be tax-deductible and the withdrawals in retirement are taxed, while Roth IRA contributions are taxed upfront and withdrawals are tax-free.

Please note that this list is not comprehensive and there are other types of retirement plans available.

What are the 4 pillars of retirement?

The four pillars of retirement are often considered to be:

- Social Security: This is a government-funded program that provides a basic level of income to retirees, as well as to disabled individuals and survivors of deceased workers.

- Personal savings: This includes any money saved in a retirement account, such as a 401(k) or individual retirement account (IRA), as well as any other savings or investments you may have.

- Employer-sponsored retirement plans: This includes traditional pension plans, as well as 401(k) plans and other types of defined contribution plans offered by employers.

- Government programs and subsidies: this includes programs such as Medicare and Medicaid, which provide healthcare coverage for retirees, as well as various subsidies and tax breaks for retirees.

It's important to note that this list is not exhaustive and there may be other types of income or support that can help you in your retirement. It's important to consult with a financial advisor to understand your retirement options and plan accordingly.

What is the 3% rule retirement?

The 3% rule of retirement is a general guideline that suggests you can withdraw 3% of your retirement savings each year and still have enough to last throughout your retirement. The idea behind this rule is that you can safely withdraw a small percentage of your savings each year while maintaining the purchasing power of your savings over time.

This rule is based on the assumption that your savings will earn a certain rate of return and that inflation will be at a certain level. For example, if you have saved $1,000,000 and assume a return of 7% and an inflation of 2% you can withdraw $30,000 (3% of $1,000,000) in the first year of your retirement and still have enough to last throughout a 30-year retirement.

It's important to note that this rule is just a general guideline and may not be appropriate for everyone. Factors such as your spending habits, how long you expect to live, and how much you have saved will all affect how much you can safely withdraw in retirement. Additionally, the rule assumes a steady withdrawal rate and returns, which may not be the case in real world, as markets could fluctuate and cause unpredictable returns. It's important to consult with a financial advisor to develop a personalized retirement plan that takes into account your specific financial situation and goals.

What is the 70 percent rule retirement?

The 70% rule in retirement is a guideline that suggests that retirees should aim to replace 70% of their pre-retirement income in order to maintain a similar standard of living in retirement. This is based on the idea that retirees will have lower expenses in retirement, such as no longer needing to save for retirement or pay for work-related expenses.

This rule is often used as a starting point to determine how much you need to save for retirement and how much you can safely withdraw each year. However, it's important to note that the 70% rule is just a rough estimate and may not be appropriate for everyone. Factors such as your spending habits, lifestyle, health, and how long you expect to live will all affect how much you actually need to replace your income in retirement.

Additionally, the rule doesn't take into account the other sources of retirement income you may have, like Social Security, pension plan, or any other savings or investments. It's important to consult with a financial advisor and to develop a personalized retirement plan that takes into account your specific financial situation and goals.

How do I create a retirement plan?

Creating a retirement plan involves several steps, including:

- Assessing your current financial situation: This includes determining your current income and expenses, as well as any assets, debts, and savings you have.

- Identifying your retirement goals: This includes determining how much income you will need in retirement and what you want to do in retirement.

- Estimating your retirement income: This includes estimating how much you will receive from Social Security, any employer-sponsored retirement plans, and any other sources of income.

- Determining your shortfall: This includes calculating the difference between your estimated income and your estimated expenses in retirement.

- Developing a savings and investment strategy: This includes determining how much you need to save each month to reach your retirement goals and deciding how to invest your savings.

- Reviewing and updating your plan regularly: Your retirement plan should be reviewed and updated regularly, as your financial situation, goals, and the market conditions are subject to change.

It's important to consult with a financial advisor to help you understand your options and create a personalized retirement plan that fits your specific financial situation and goals. An advisor can provide you with professional advice and help you create a plan that takes into account your risk tolerance, time horizon, and investment goals.

F.A.Q on Retirement Plan:

What is a retirement plan?

A retirement plan is a financial plan designed to help individuals save and invest money for their retirement. These plans typically involve setting aside a portion of income and investing it in various financial instruments.

What are the different types of retirement plans?

The most common types of retirement plans are 401(k)s, IRAs, and pension plans. 401(k)s and IRAs are individual retirement accounts that allow individuals to save for retirement on their own, while pension plans are typically offered by employers as part of their employee benefits packages.

When should I start saving for retirement?

It's best to start saving for retirement as early as possible. The earlier you start, the more time your money has to grow and compound.

How much should I save for retirement?

The amount you should save for retirement depends on your retirement goals, lifestyle, and expected expenses. As a general rule, financial experts recommend saving at least 15% of your income for retirement.

What are the tax benefits of a retirement plan?

Retirement plans offer tax benefits in the form of tax-deferred contributions, meaning you don't have to pay taxes on the money you contribute until you withdraw it during retirement. Additionally, some retirement plans offer tax-free growth, meaning you won't have to pay taxes on the money your investments earn.

What happens to my retirement plan if I change jobs?

If you change jobs, you may be able to roll over your retirement plan into a new plan or an IRA. This allows you to continue growing your retirement savings without incurring taxes or penalties.

How do I choose the right retirement plan for me?

Choosing the right retirement plan depends on your personal financial goals and situation. Consider factors such as your income, employer benefits, and investment preferences when choosing a retirement plan.

Can I make changes to my retirement plan?

Yes, you can make changes to your retirement plan. You can adjust your contributions, change your investment allocation, and make other changes as needed to help you achieve your retirement goals.

What should I do if I'm behind on my retirement savings?

If you're behind on your retirement savings, consider increasing your contributions, adjusting your investment strategy, or working with a financial advisor to create a plan that can help you catch up.

When can I start withdrawing from my retirement plan?

You can start withdrawing from your retirement plan after you reach the age of 59 and a half. If you withdraw before this age, you may be subject to taxes and penalties.

Author : Uttam Bisht

14 February, 2024 | 11:06 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

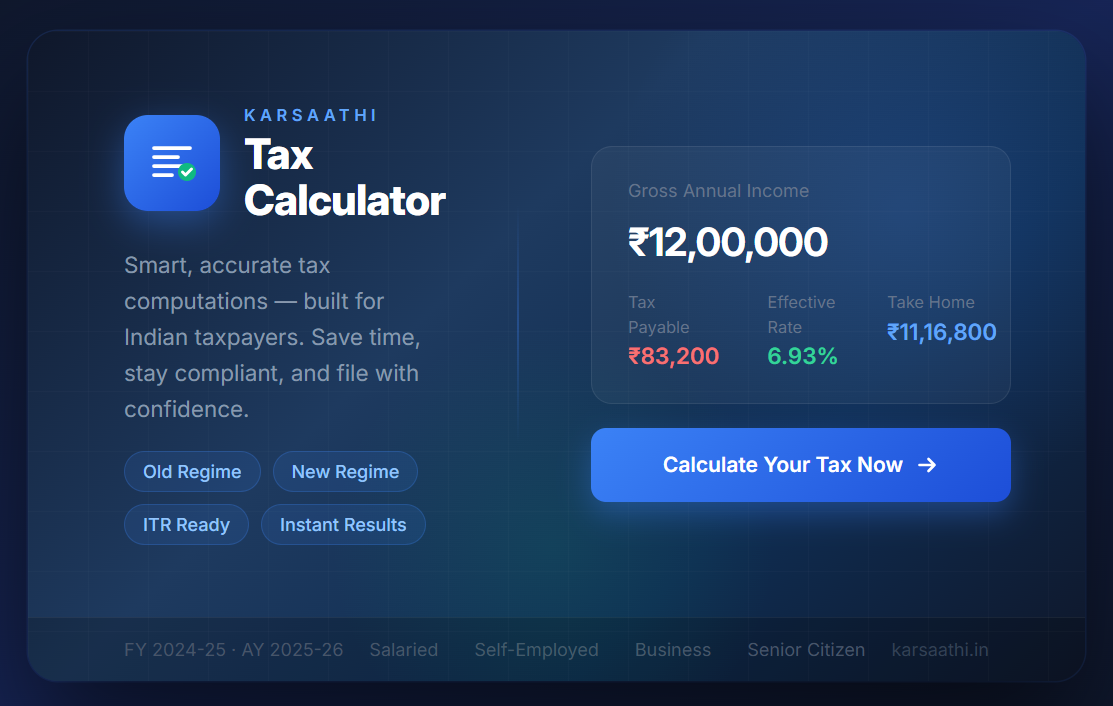

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM