28 Most common mistake while filing ITR

Filing your Income Tax Return (ITR) accurately and timely is crucial to maintain compliance with tax laws and ensure peace of mind. However, many taxpayers inadvertently make mistakes that can lead to complications, penalties, or delays in processing.

Some mistakes are to be taken care of while filing an income tax return:

1: Not reporting all income sources

The IT department is likely to see your failure to disclose all of your sources of income on your income tax return as income concealment, and you could be charged a tax and/or penalty.

2: Don’t forget to declare more than 1 house

If you own more than one home, it must be taken into account when calculating your income tax. The second most frequent error people make when filing tax returns is failing to declare such properties.

3: Never report falsified income sources

Even while this might not be considered a mistake, many tax advisors encourage their clients to file surge returns in order to maximise their tax benefits.

4: Providing incorrect personal details

A lot of people have trouble filing income tax returns because their postal addresses, phone numbers, and email addresses are erroneous or invalid.

5: Not reporting interest income from Saving Banks

When filing tax returns for the previous fiscal year (for which the return is being submitted), an individual is required to disclose all interest incomes received or accrued to him during that period. Under the heading "Income from other sources," people frequently neglect to include interest from savings bank accounts, fixed deposits, recurring deposits, etc. While interest on fixed and recurring deposits is completely taxed.

6: Not reporting income from the previous employers

If you changed jobs during a fiscal year, the income from your old job must be included with the income from your new employment when submitting your income tax return. Your TDS certificates, Form 16 and Form 26AS will all show a discrepancy if any income (from a prior job) is not recorded. Taxman, this will inevitably lead you to your home. The consequences for not clubbing your income remain the same.

Should I mention all bank accounts in ITR?

7: Not reporting all bank accounts

Every bank account that a taxpayer has in the previous year must be disclosed in the income tax return. In the past, you were only had to specify one bank account where you wanted your income tax refund, if any, to be credited.A person must record all sources of income and file an ITR using the appropriate form for him, as required by tax rules. If he submits it using the incorrect form, his submitted return will be deemed "defective," and he will be required to submit a new ITR using the proper form. The assessing officer will consider the return to be invalid if the flaw is not fixed within the allotted period.

8: Carelessness in choosing the right ITR form

A person must record all sources of income and file an ITR using the appropriate form for him, as required by tax rules. If he submits it using the incorrect form, his submitted return will be deemed "defective," and he will be required to submit a new ITR using the proper form. The assessing officer will consider the return to be invalid if the flaw is not fixed within the allotted period.

9: Ignoring the form 26AS &TDS Certificates

The Form 26AS of the relevant PAN contains information on the tax deducted or collected by an entity, which aids in locating any inconsistencies or mistakes. Such TDS credits must be compared to the income reported in the ITR in order to be accurate. In the form 26AS, which is a consolidated tax statement and a proof of tax deducted on your behalf, he should double-check that he received the proper tax credit.

10: Not Verify your tax return timely

The next step is to verify your income tax return after you have successfully filed it. Once it has been authenticated, the Income Tax Department will begin processing your return. Returns that have been filed and confirmed are processed for refunds, if any. You don't need to send the actual ITR-V once you've successfully re-verified your ITR using net banking. However, if you do not want to e- verify, you will have to send the physical ITR-V. You must transmit the actual ITR-V if you choose not to e-verify, nevertheless.

11: Not filing income tax returns

Many persons who either do not have income that is below the tax-exempt income level or who do have exempted income, such as agricultural income, dividends, or capital gains, fail to file their income tax returns. A person may experience a loss in their business or in the stock market and decide not to file an ITR because they believe that they are not required to do so. However, they should carefully review the applicable laws in each situation and weigh the advantages of filing an ITR even if there is no income tax.

12: Not reporting tax-free incomes

Even if portion of your income is tax-free, it is your responsibility as a taxpayer to disclose it fully. Your ITR needs to include any interest from bonds exempt from taxes or the provident fund that you received throughout the fiscal year. However, there are a number of parts of the Income Tax Act that allow you to claim an exemption on these. These exempt incomes must be disclosed in the ITR's "Exempt Income" schedule.

13: Not disclosing Foreign Assets

All foreign assets must be disclosed under the government's stringent anti-money laundering regulations. You must ensure that you have updated all such information in your ITR in order to avoid breaking the law.

14: Giving incomplete KYC or incorrect residential status

You must include accurate information regarding your name, residence, bank account number, IFSC code, Aadhaar, PAN, and assets details to ensure a smooth processing of your ITR and a prompt refund.

15: Picking the wrong year for return

Regarding the year of filing their returns, people frequently become confused. The year for which you are filing your ITR must be specified clearly. The simplest method is to think of the fiscal year in which your money was earned as the Previous Year. Assessment year refers to the year in which your income will be determined and your return will need to be completed. The Assessment Year in the current situation is 2021–2022, while the Previous Year is 2020–21.

16: Failing to revise your income

Once you have finished submitting your taxes, you must correct any errors you may have made. You must submit the amended return in order to correct your error. You are able to submit an amended return in accordance with current tax legislation.

17: Filing incorrect and incomplete bank details

Because of erroneous personal information, including name, address, bank account number, and IFSC code, many refunds are not completed each year. Many taxpayers mistakenly enter incorrect bank information, and these frequent errors in income tax return filing might delay your tax refund. All refunds of income taxes are wired to the account by the Income Tax Department. Always provide accurate bank account information for an active account on your income tax return. In contrast to prior years, a taxpayer is now required to provide information regarding all bank accounts owned by him throughout the year.

18: Not checking the bank statements

One should always check their bank statement to determine the amount of any gifts received, interest received, or other income obtained because all incomes received during a specific year must be disclosed in income tax returns. It is now essential to precisely list the exact incomes received because ITR forms now ask for the number of all active bank accounts.

19: Not reporting interest received on income tax refunds

Form 26AS can be used to track interest payments on tax refunds, which you must include as income from other sources when completing your income tax return.

20: Not clubbing incomes

The Income Tax Act states that the taxpayer may be forced to combine the income of his minor kid or spouse with his own income in certain circumstances and pay taxes as a result. Children under the age of 18 who are earning an income are considered minors, and their earnings must be combined with their parents' earnings. However, the income tax agency grants each child a Rs. 1500 exemption. For instance, if a child's name is used to open an FD, the child's parent is required to disclose the interest income to the income tax department.

21: Late Filing of income tax return

The phrase "all's well that ends well" may not be accurate when completing an income tax return. Even if filing an income tax return after the deadline is equivalent to doing so on time, there are several rights that are lost if the return is filed late. Losses are not carried over to the following year. There will be penalties for late filing. In the event of a tax liability, additional interest will also be due. The refund process is also delayed.

22: Not keeping evidence of deductions claimed in income tax return

It is necessary to keep records, evidence, and proofs of all expenses and investments that are claimed as deductions under Chapter VIA (such as child tuition fees, LIC premiums, PPF contributions, and medical insurance policies). The disallowance of such deductions and an increase in tax liability at the time of scrutiny assessment might result from claiming a deduction without having sufficient supporting documentation. Therefore, either provide proof for a specific spending or investment, or refrain from claiming a deduction for it. After the conclusion of the year in which the return is filed, your case may be examined for income tax purposes for up to 6 years. Records must therefore be preserved for 7 years.

23: Not Paying Advance Tax/ Self-Assessment Tax

TDS is often taken out of salary income and interest revenue that is received from the bank. TDS on interest income, however, may occasionally be deducted at a rate of 10% or not at all if the person is in the 30% tax bracket. Therefore, a tax that is additionally owed in this situation must be computed and paid as an advance tax. Additionally, determine your tax liability for rental revenue and pay your advance tax in accordance with the legislation. Self-Assessment tax is paid when a return is filed. Additionally, the Income Tax Return must include all information on self-assessment tax payments and advance tax payments.

24: Not reporting capital gains on switching units of mutual funds

These transactions are not shown in the bank statements, and the income tax return makes no mention of them either. Since these transfers do not go through the taxpayer's bank account, the profit made on them is not disclosed. It is advisable to disclose the change in the income tax return because switching or moving from one scheme to another may result in profit or loss.

25: Fake Invoices/ giving wrong disclosure

Fake bills typically pertain to deductions allowed under Sections 80C and 80D of the Income Tax Act, such as receipts from LICs, medical expenses, or rent payments, among others. The HRA (House Rent Allowance) should not be claimed using fictitious invoices or rent receipts. In some cases, people exaggerated the worth of the invoices despite the fact that they were less expensive in reality.

By reviewing the bank information or cross-checking with the vendor, landlord, etc., the Income Tax department can quickly find the source of these fictitious bills.

26: Incorrect Residential Status

One of the most frequent errors in tax filing is choosing the wrong residence status. The two parameters for the residence status are 60 days and 182 days. The taxpayer must first ensure that their residential status is accurate because this will affect the range of income that is taxable in India. For instance, an Indian resident is subject to taxation on all of their income, including their international income. However, only the income that accrues, arises, or is assumed to arise in India is taxed in the case of non-residents.

27: Not claiming correct Section 80 deductions

Some donations are accepted at 100%, while others are accepted at 50%. Similar to how certain investment returns are tax-free but others are taxed. Therefore, such a deduction should be claimed cautiously to avoid income tax department scrutiny.

28: Not submitting Requisite Income Tax Forms

The taxpayer must submit specific forms prior to filing returns in order to claim certain exemptions. For instance, form 10E must be filed if you received salary arrears during the financial year and need assistance with the increased tax burden under section 89(1). Another situation is when a taxpayer wishes to apply for relief from overseas taxes and must submit Form 67. You must submit these forms prior to submitting your income tax returns in order to receive certain exemptions or benefits. The person will not be able to claim the relief if these forms are not filled out. Additionally, this will raise the likelihood of receiving a tax notification.

Frequently Asked Questions:

What is an Income Tax Return (ITR)?

An Income Tax Return (ITR) is a form used by taxpayers to file their income and tax details with the government. It provides information about your income earned during a financial year and the taxes paid on it.

What are some common mistakes to avoid when filing ITR?

Common mistakes include incorrect personal details, forgetting to report all sources of income, using the wrong ITR form, miscalculating tax liability, and not verifying the return.

What should I do to avoid making mistakes in my ITR?

Double-check all personal details, gather all necessary documents, accurately report all income sources, choose the correct ITR form, and utilize online tools or consult a tax professional if needed.

How can I ensure that I choose the correct ITR form?

The correct ITR form depends on your income sources and type of taxpayer (individual, HUF, company, etc.). The Income Tax Department provides guidelines to help you choose the appropriate form. You can also seek assistance from a tax consultant.

What are some common errors in reporting income?

Common errors include failing to report income from interest, dividends, capital gains, rental income, or freelance work. Ensure you account for all sources of income earned during the financial year.

What documentation should I gather before filing my ITR?

Gather documents such as Form 16 (for salaried individuals), bank statements, investment proofs, property documents, rent receipts, and any other relevant financial documents related to your income and expenses.

How can I avoid errors in calculating tax liability?

Double-check your calculations, use online tax calculators or professional assistance, ensure you've applied all eligible deductions and exemptions, and stay updated on changes in tax laws.

What is the importance of verifying my ITR?

Verifying your ITR is crucial to complete the filing process. It confirms that the information provided in the return is accurate and authentic. Failure to verify can lead to your return being considered invalid.

What are the different methods of verifying my ITR?

You can verify your ITR electronically through methods such as Aadhaar OTP, net banking, or by sending a signed physical copy to the Centralized Processing Center (CPC) within 120 days of e-filing.

What should I do if I discover an error after filing my ITR?

If you discover an error after filing, you can rectify it by filing a revised return within the specified time limit. The earlier you rectify the error, the better it is to avoid penalties or scrutiny from tax authorities.

Can I claim deductions and exemptions if I forget to include them in my original return?

Yes, if you've missed claiming deductions or exemptions in your original return, you can still claim them by filing a revised return

What are some common mistakes related to deductions and exemptions?

Common mistakes include claiming ineligible deductions, failing to provide proper documentation for claimed deductions, and overlooking certain exemptions available under the Income Tax Act.

How can I ensure accurate reporting of investments and assets?

Keep detailed records of all investments and assets, including purchase cost, sale proceeds, and any applicable gains or losses. Ensure you report these accurately in your ITR to avoid discrepancies.

What is the penalty for filing an incorrect or late ITR?

Penalties for incorrect or late filing can include fines and interest charges. It's essential to file your ITR accurately and within the specified deadline to avoid such penalties.

How can I rectify errors in my PAN or other personal details?

If you've made errors in your PAN or other personal details, you can rectify them by filing a rectification request online or by contacting the Income Tax Department directly.

What should I do if I receive a notice from the Income Tax Department regarding discrepancies in my ITR?

If you receive a notice, carefully review the discrepancies mentioned and respond promptly. Provide any additional information or documentation required to resolve the issue.

Can I file my ITR without a Form 16?

Yes, you can file your ITR without a Form 16 by using other relevant documents such as salary slips, bank statements, and Form 26AS,which provides details of tax deducted at source (TDS).

What are some common errors related to TDS?

Common errors include mismatched TDS details, failure to report TDS deducted, or claiming excess TDS than what is available in Form 26AS. Verify all TDS details carefully before filing your ITR.

How can I ensure accurate reporting of foreign assets or income?

If you have foreign assets or income, ensure you comply with reporting requirements as per Indian tax laws. Familiarize yourself with Foreign Asset Tax Compliance Act (FATCA) and report all relevant details in your ITR.

What are some common errors while filing ITR for freelancers or self-employed individuals?

Common errors include improper calculation of business income, failure to maintain proper records of expenses, and overlooking deductions available to self-employed individuals. Keep detailed records and seek professional advice if needed.

Can I claim deductions for donations made to charitable organizations?

Yes, donations made to eligible charitable organizations are eligible for deductions under Section 80G of the Income Tax Act. Ensure you obtain proper receipts and documentation for claimed donations.

What is the difference between e-verification and physically signing the ITR-V?

E-verification involves digitally signing your return using methods such as Aadhaar OTP or net banking, while physically signing the ITR-V involves sending a signed copy of the ITR acknowledgment (ITR-V) to the CPC. Both methods serve to verify the authenticity

Is it necessary to keep copies of filed ITR and supporting documents?

Yes, it is essential to keep copies of filed ITR and all supporting documents for a minimum of six years from the end of the relevant assessment year. These documents may be required for future reference or in case of tax scrutiny.

What should I do if I encounter technical issues while e-filing my ITR?

If you encounter technical issues, such as website crashes or errors during e-filing, you can seek assistance from the Income Tax Department's helpdesk or consider using alternative e-filing platforms.

Can I file my ITR on behalf of someone else?

Yes, you can file ITR on behalf of someone else if you are authorized to do so. This authorization can be through a power of attorney or other legal means. Ensure you have all necessary documentation and permissions before filing on someone else's behalf.

What is the importance of reviewing my ITR before submission?

Reviewing your ITR before submission helps identify and rectify any errors or discrepancies. It ensures the accuracy of the information provided and reduces the likelihood of receiving notices or penalties from the tax authorities.

How can I stay updated on changes in tax laws and filing procedures?

Stay informed by regularly checking updates from the Income Tax Department's official website, subscribing to newsletters or alerts, and consulting with tax professionals who can provide guidance on changes relevant to your tax situation.

What should I do if I need assistance with filing my ITR?

If you need assistance, consider consulting a qualified tax professional or using online tax filing platforms that provide guidance and support throughout the filing process. They can help ensure accuracy and compliance with tax laws.

Author : Uttam Bisht

14 February, 2024 | 11:24 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

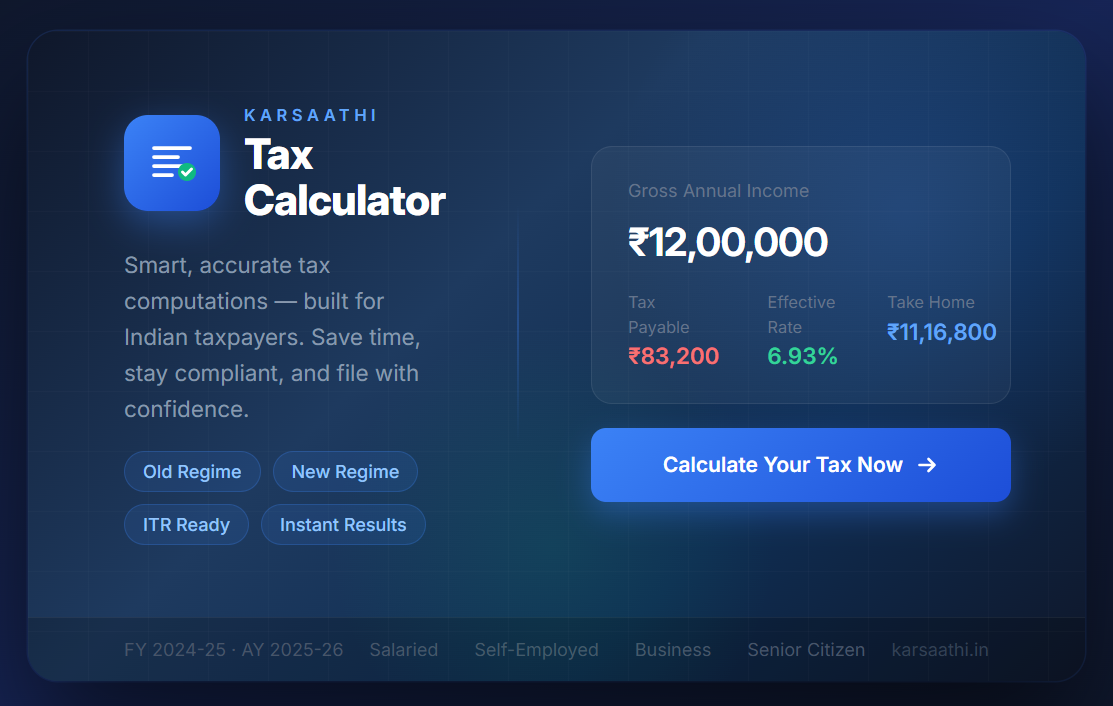

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

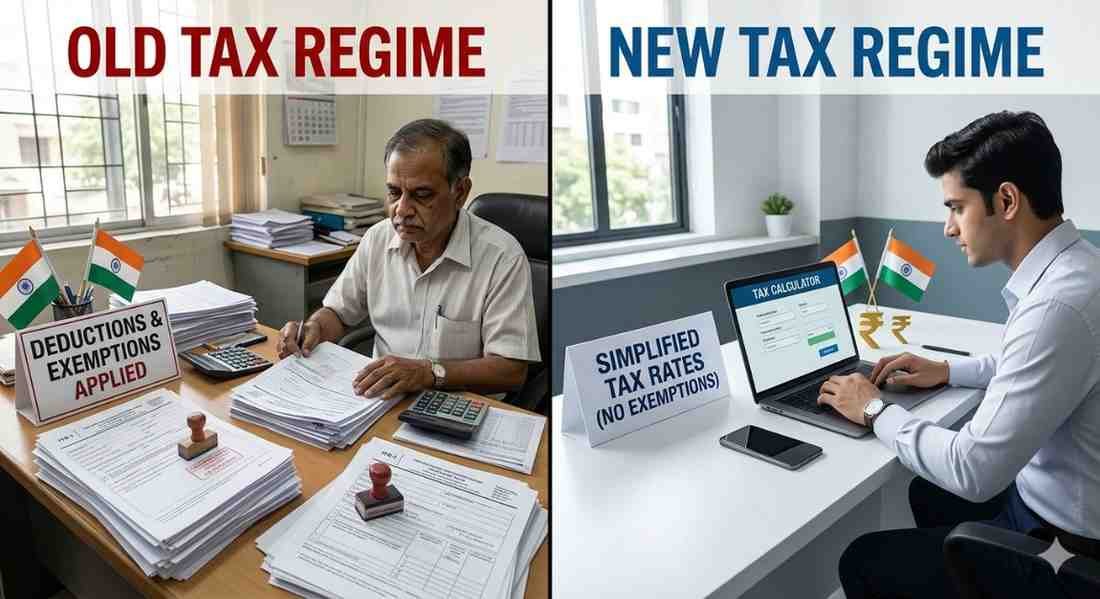

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM