Deductions from income from house property for interest payments U/S 24

Income chargeable under the head "Income from house property" shall be computed after making the following deductions, namely:

a sum equal to thirty per cent of the annual value

where the property has been acquired, constructed, repaired, renewed or reconstructed with borrowed capital, the amount of any interest payable on such capital:

Provided that in respect of property referred to in sub-section (2) of section 23, the amount of deduction 80[or, as the case may be, the aggregate of the amount of deduction] shall not exceed thirty thousand rupees :

Provided further that where the property referred to in the first proviso is acquired or constructed with capital borrowed on or after the 1st day of April, 1999 and such acquisition or construction is completed within five years from the end of the financial year in which capital was borrowed, the amount of deduction 81[or, as the case may be, the aggregate of the amounts of deduction] under this clause shall not exceed two lakh rupees.

Where the property has been acquired or constructed with borrowed capital, the interest, if any, payable on such capital borrowed for the period prior to the previous year in which the property has been acquired or constructed, as reduced by any part thereof allowed as deduction under any other provision of this Act, shall be deducted under this clause in equal installments for the said previous year and for each of the four immediately succeeding previous years

Provided also that no deduction shall be made under the second proviso unless the assess furnishes a certificate, from the person to whom any interest is payable on the capital borrowed, specifying the amount of interest payable by the assess for the purpose of such acquisition or construction of the property, or, conversion of the whole or any part of the capital borrowed which remains to be repaid as a new loan.

For the purposes of this proviso, the expression "new loan" means the whole or any part of a loan taken by the assess subsequent to the capital borrowed, for the purpose of repayment of such capital

Provided also that the aggregate of the amounts of deduction under the first and second provisos shall not exceed two lakh rupees.

FOR EXAMPLE :

AMIT works in Gurgaon in an company. He recently purchased a house in NOIDA. He purchased this property jointly with his father. AMIT has taken a loan of Rs 25 lakhs and his father is not a co-borrower in this loan. His parents live in this house currently.

AMIT's EMI of Rs.20,000 began in APRIL 2018

AMIT's income from house property is zero because his parents live in it.

Let's see how AMIT can save on tax on his home loan when he files his income tax return this year.

The total of EMIs for the financial year 2018-19 is Rs. 2,40,000 (20000 X 12 months). This amount includes a payment of Rs.40,000 towards principal and Rs 2,00,000 towards interest.

AMIT's income from house property is zero because his parents live in it. The I-T Department considers it a self-occupied house.

Since there is no income from his self occupied house property and as a result of claiming a deduction towards interest of Rs. 2,00,000 under Section 24, AMIT makes a loss under the head house property in his Income Tax Return.

AMIT can subtract this loss from his taxable income this year. He can also claim his principal repayment amount of Rs. 40,000 under Section 80C. But he cannot sell this house for a period of 5 years, which ends on 31 March 2023.

Author : Uttam Bisht

09 February, 2024 | 03:49 AM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

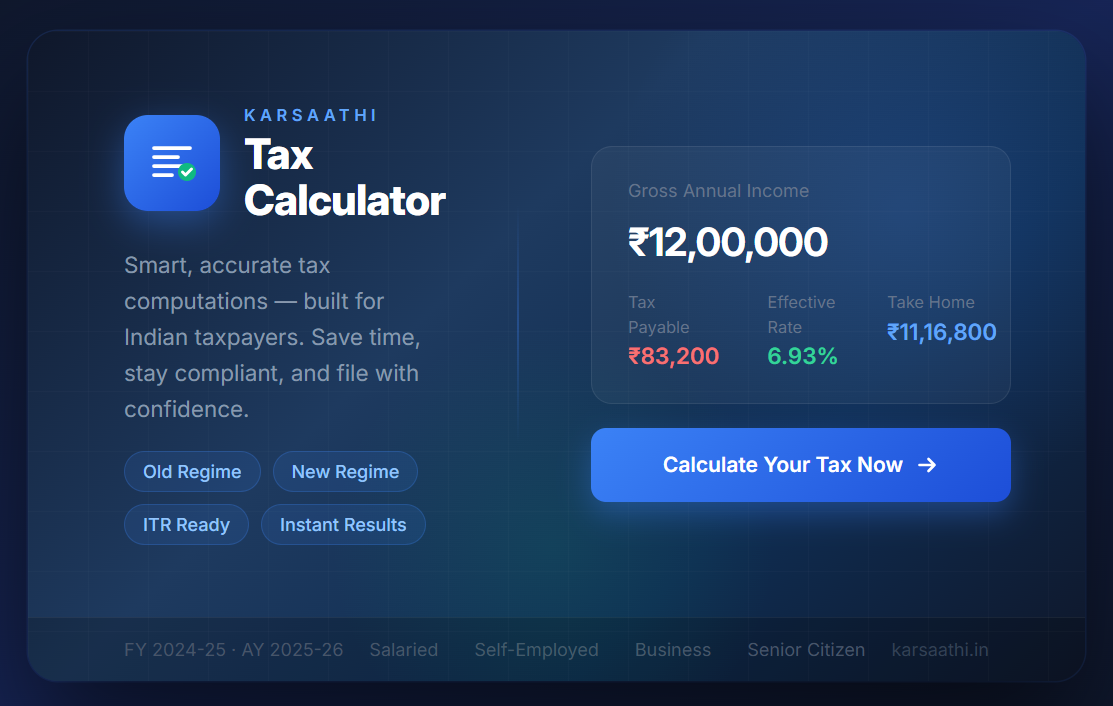

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

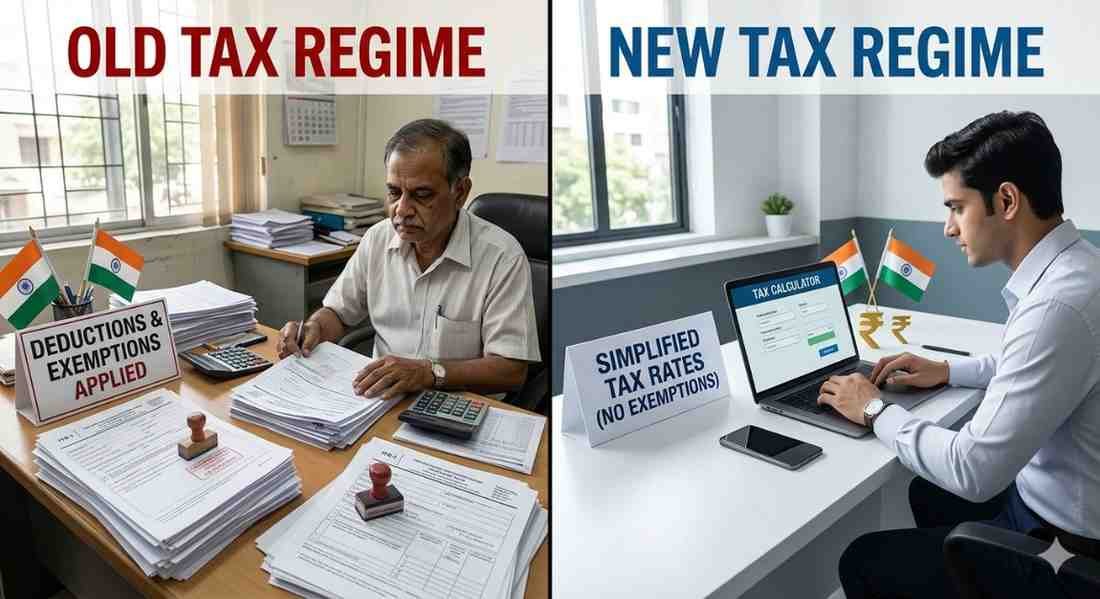

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM