Is PPF a good tool for future retirement planning?

A public provident fund (PPF) account can be a good tool for long-term retirement planning as it offers several benefits that make it an attractive investment option. Some of the key benefits of investing in a PPF account include:

- Security: PPF is a government-backed investment, which makes it a relatively secure option.

- Tax benefits: Contributions to a PPF account are eligible for tax deductions under Section 80C of the Income Tax Act, up to a maximum of INR 1.5 lakhs per financial year. In addition, the interest earned on a PPF account is tax-free.

- Flexibility: PPF accounts have a long-term investment horizon of 15 years, but they can be extended in blocks of 5 years. This allows you to choose the investment horizon that best meets your needs.

- Attractive interest rate: PPF accounts offer an attractive interest rate, which is set by the government. The interest rate on PPF accounts is currently 7.1% p.a.

Overall, a PPF account can be a good tool for long-term retirement planning as it offers a combination of security, tax benefits, flexibility, and an attractive interest rate. However, it is important to keep in mind that PPF is a long-term investment and the interest rate may fluctuate over time. It is always a good idea to consult with a financial advisor before making any investment decisions.

Is PPF a good investment for the future?

Public Provident Fund (PPF) is considered a safe investment option in India due to its sovereign guarantee and fixed rate of return. However, its returns may not be as high as some other investment options, such as equity or mutual funds, over the long term. Ultimately, the suitability of PPF as an investment option depends on an individual's financial goals, risk tolerance, and investment horizon. It is advisable to consult a financial advisor before making any investment decisions.

Is PPF good for long term investment?

Public Provident Fund (PPF) can be a good option for long-term investment for some individuals, as it offers tax benefits and a fixed rate of return that is guaranteed by the government. However, it is important to consider the following factors before investing in PPF:

- Lock-in period: PPF has a lock-in period of 15 years, which means you cannot withdraw the money before maturity.

- Low return: The rate of return on PPF is relatively low compared to other investment options.

- Limited contribution: The maximum contribution to PPF is limited to INR 1.5 lakhs per financial year.

In conclusion, PPF can be a good option for long-term investment for those looking for a low-risk investment option with a guaranteed return and tax benefits. However, it may not be suitable for those who need access to their money in the short term or are looking for higher returns. Before making any investment, it is advisable to consider your financial goals, risk tolerance, and investment horizon.

What is the best option for retirement planning?

There is no one-size-fits-all answer to what is the best option for retirement planning, as it depends on an individual's financial situation, goals, risk tolerance, and other factors. Here are some commonly used options for retirement planning:

- Employer-sponsored retirement plans (e.g., 401(k), 403(b), pension)

- Individual retirement accounts (IRAs)

- Annuities

- Stocks, bonds, mutual funds

- Real estate investments

It is recommended to consult a financial advisor to determine the best plan for your unique circumstances and to create a comprehensive retirement strategy.

What is difference between PF EPF and PPF?

Can I have both EPF and PPF?

I think it is a great idea to invest in both PPF and EPF to help you reach your long-term financial goals, especially retirement, and to help you build up a sizable corpus for your retirement.

Which is better PPF or EPF?

What are some interesting retirement plans? Rather than sitting at home and living on pension, how can one make the best use of this 'holiday'?

Retirement can be a time to relax and enjoy the fruits of your labor, but it can also be an opportunity to pursue new interests and activities that you may not have had time for while you were working. Here are a few ideas for how you can make the most of your retirement:

- Travel: Retirement can be a great time to explore new places and cultures. Consider planning a trip to a destination you have always wanted to visit or take a cruise to see multiple destinations in one trip.

- Volunteer: Giving back to your community can be a rewarding way to spend your time in retirement. Consider volunteering with a local organization or non-profit that aligns with your interests and values.

- Take up a hobby: Retirement can be a great time to try something new or rediscover a hobby you used to enjoy. Consider taking up a creative pursuit, such as painting or writing, or try something more physical, such as golf or dancing.

- Learn something new: Keep your mind active by learning a new skill or subject. Consider taking a class or workshop at a local community center or university, or consider taking an online course.

- Stay active: Staying physically active is important for maintaining good health and overall well-being. Consider joining a fitness class or club, or consider taking up a sport or outdoor activity that you enjoy.

- Spend time with loved ones: Retirement can be a great time to strengthen relationships with friends and family. Consider planning regular get-togethers or trips with loved ones, or consider volunteering or working on a project together.

Overall, the key to making the most of your retirement is to find activities that bring you joy and fulfillment. Don't be afraid to try something new and be open to new experiences.

Which is better for retirement PPF or NPS?

Both the Public Provident Fund (PPF) and the National Pension System (NPS) can be good options for retirement savings in India. However, they have some differences that you should consider when deciding which one is best for you.

Some key points to consider:

- Contribution limits: The maximum annual contribution to a PPF account is Rs. 1.5 lakhs. In comparison, there is no limit on the amount you can contribute to an NPS account.

- Tax benefits: Contributions to a PPF account are tax-deductible under section 80C of the Income Tax Act, up to a limit of Rs. 1.5 lakhs. In addition, the interest earned and the maturity proceeds are tax-free. NPS contributions are also tax-deductible, but the tax treatment of the maturity proceeds depends on the proportion of the corpus that is used to purchase an annuity.

- Investment options: PPF investments are restricted to a fixed set of government securities, while NPS offers a range of investment options including equity, corporate bonds, and government securities.

- Withdrawal rules: PPF account holders can make partial withdrawals from the seventh financial year, and the account matures after 15 years. The NPS has more flexible withdrawal rules, allowing you to make partial withdrawals starting at age 60, with the balance used to purchase an annuity.

Ultimately, the choice between a PPF and an NPS will depend on your specific financial situation and retirement goals. It's a good idea to carefully consider the pros and cons of each option and seek professional financial advice before making a decision.

What are the disadvantages of PPF?

The Public Provident Fund (PPF) is a long-term savings scheme that is offered by the government of India. It is a popular investment option because it offers tax benefits, a stable rate of return, and the security of being backed by the government. However, there are also some disadvantages to consider:

- Low returns: The interest rate on PPF investments is set by the government and can fluctuate over time. While the rate has historically been higher than many other fixed-income investments, it has also been quite low in recent years. This means that the returns on a PPF investment may not keep pace with inflation.

- Long lock-in period: PPF investments have a lock-in period of 15 years, during which time you are not allowed to make any withdrawals. This can be a disadvantage if you need access to your money before the end of the lock-in period.

- Partial withdrawal restrictions: While PPF account holders are allowed to make partial withdrawals starting from the seventh financial year, these are subject to certain conditions and restrictions. For example, you are only allowed to make one withdrawal per year and the amount must not exceed your contributions in the preceding four years.

- Limited investment options: PPF investments are restricted to a fixed set of government securities, which means you do not have the flexibility to choose where your money is invested. This can be a disadvantage if you are looking for more control over your investment portfolio.

It's important to carefully consider the potential disadvantages of a PPF investment before deciding if it is the right option for you.

How can I check my PF balance?

There are several ways to check your Provident Fund (PF) balance online:

- Through the EPFO Portal: Go to the official website of the Employees' Provident Fund Organization (EPFO) at https://www.epfindia.gov.in/ and log in to your account. Once logged in, you can view your current PF balance under the "Passbook" section.

- Through the UMANG app: Download the UMANG app from the App Store or Google Play. Once the app is installed, register for an account using your mobile number and Aadhaar number. After registration, you can log in and view your current PF balance under the "EPFO" section.

- Through the Umang website: Go to the official website of Umang at https://web.umang.gov.in/web/#/ and log in to your account. Once logged in, you can view your current PF balance under the "EPFO" section.

- Through SMS: You can also check your PF balance by sending an SMS to the EPFO's designated number. The format of the SMS is "EPFOHO UAN ENG", where UAN is your Universal Account Number and ENG is the preferred language (for example, Hindi, Bengali, etc.).

Keep in mind that you will need your Universal Account Number (UAN) to access your PF balance information. If you don't have your UAN, you can get it from your employer or by visiting the EPFO's website.

How can I withdraw my PF online?

Withdrawing your Provident Fund (PF) online is a quick and easy process that can be done from the comfort of your own home. Here are the steps you can follow to withdraw your PF online:

- Go to the official website of the Employees' Provident Fund Organization (EPFO) at https://www.epfindia.gov.in/

- Register for an account if you don't already have one. You will need your Universal Account Number (UAN) and other personal information to register.

- Log in to your account and navigate to the "Online Services" tab.

- Click on the "Claim (Form 31, 19 & 10C)" option.

- Fill out the necessary details such as your bank account information and the reason for withdrawal.

- Upload any necessary documents, such as your PAN card and Aadhaar card.

- Submit the form and wait for the EPFO to process your request. You will receive an SMS or email when your request has been approved.

- Once approved, your PF amount will be credited to your bank account.

Keep in mind that you may be required to complete certain conditions like working for at least 2 months with the current employer, to withdraw your PF.

It's also worth noting that If you have completed five years of service, you can withdraw the full amount of your EPF account balance, but if you have completed less than five years of service, you can only withdraw the employer's contribution and interest.

Can we withdraw pension contribution from PF?

Yes, it is possible to withdraw your pension contribution from your Provident Fund (PF) account, but there are certain conditions that must be met.

According to the Employees' Provident Fund Organization (EPFO), you can withdraw your pension contribution if:

- You have completed 58 years of age or more.

- You have completed 10 years of service or more.

- You are not employed at the time of withdrawal.

If you meet these conditions, you can withdraw your pension contribution by submitting a Form 10C and Form 19 to the EPFO. You will also need to provide proof of age and service, such as your birth certificate or service certificate.

It's important to note that once you withdraw your pension contribution, you will not be eligible for a monthly pension from the Employees' Pension Scheme (EPS) once you reach the age of 58.

Additionally, if you withdraw your pension contribution before completing 10 years of service, you will not be eligible for the EPS pension at all.

It's important to consider carefully the long-term impact before making the decision of withdrawing your pension contribution from your PF account. It's always a good idea to consult a financial advisor before taking any such decisions.

Is PPF a good investment for child?

Public Provident Fund (PPF) can be a good investment option for a child as it offers a number of benefits, including tax benefits, guaranteed returns, and a long-term investment horizon. However, it is important to keep the following factors in mind before investing in PPF for a child:

- Age restrictions: Only individuals who are at least 18 years of age and have a PAN card can open a PPF account.

- Limited contribution: The maximum contribution to PPF is limited to INR 1.5 lakhs per financial year.

- Lock-in period: PPF has a lock-in period of 15 years, which means the invested money cannot be withdrawn before maturity.

- Low return: The rate of return on PPF is relatively low compared to other investment options.

In conclusion, PPF can be a good option for long-term investment for a child if the child's guardian is looking for a low-risk investment option with a guaranteed return and tax benefits. However, it may not be the best option for a child if the guardian is looking for higher returns or greater flexibility. Before making any investment decision, it is important to consider the child's financial goals, the guardian's risk tolerance, and the investment horizon.

Can parents claim PPF deduction for child?

Yes, parents can claim PPF deduction for their child by opening a Public Provident Fund (PPF) account in the child's name. As a legal guardian, the parent can make contributions to the child's PPF account and claim a tax deduction under section 80C of the Income Tax Act, 1961.

It is important to note that the maximum contribution to PPF is limited to INR 1.5 lakhs per financial year and the child must be at least 18 years old and have a PAN card to open a PPF account. Additionally, the PPF has a lock-in period of 15 years, during which the invested money cannot be withdrawn before maturity.

In conclusion, parents can claim PPF deduction for their child by opening a PPF account in the child's name, but it is important to consider the child's age, tax implications, and investment horizon before making any investment decisions.

Author : Uttam Bisht

14 February, 2024 | 10:57 PM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

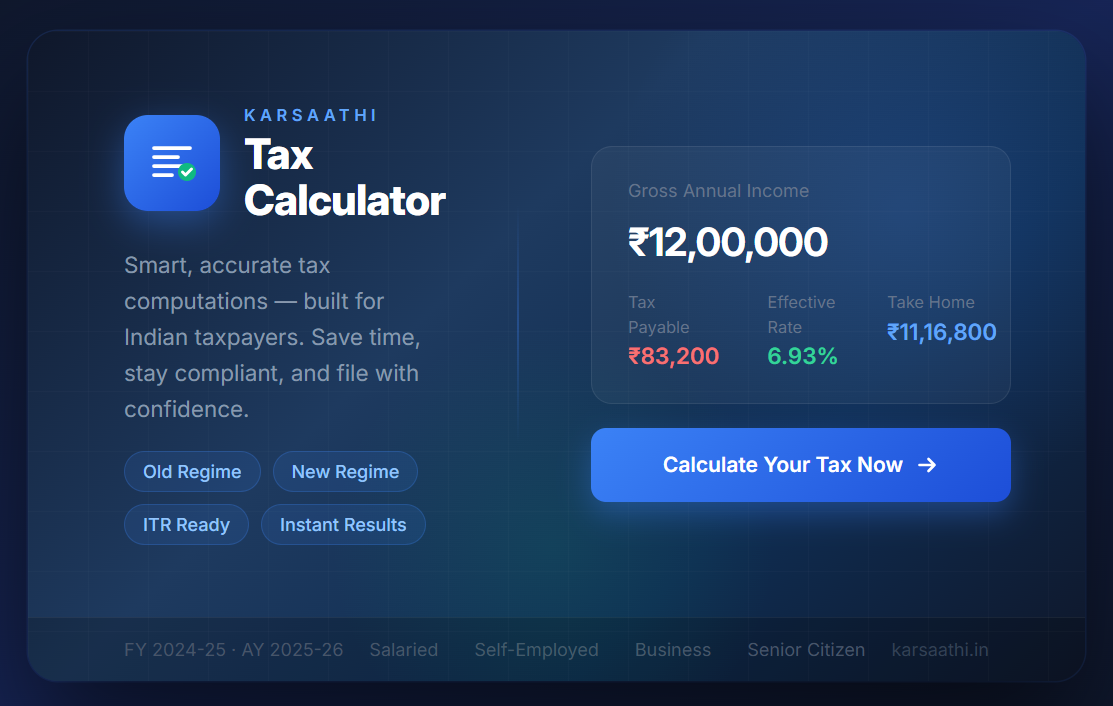

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM