Author :

09 August, 2026 | 11:53 AM

Mr. Uttam Bisht is a partner with the Delhi Branch of the firm. He has more than 8 years of experience and specializes in Statutory Audit. Expertise in Tax audit of various enterprises. Extpertise internal audit of Private enterprises. Audit planning through business understanding, preliminary analytical procedures, determining materiality levels, and preparation of audit program and pre-audit checklist . He is well conversant with the auditing standards issued by ICAI. .

Tags

Recent Blogs

28 May, 2026 | 04:34 PM

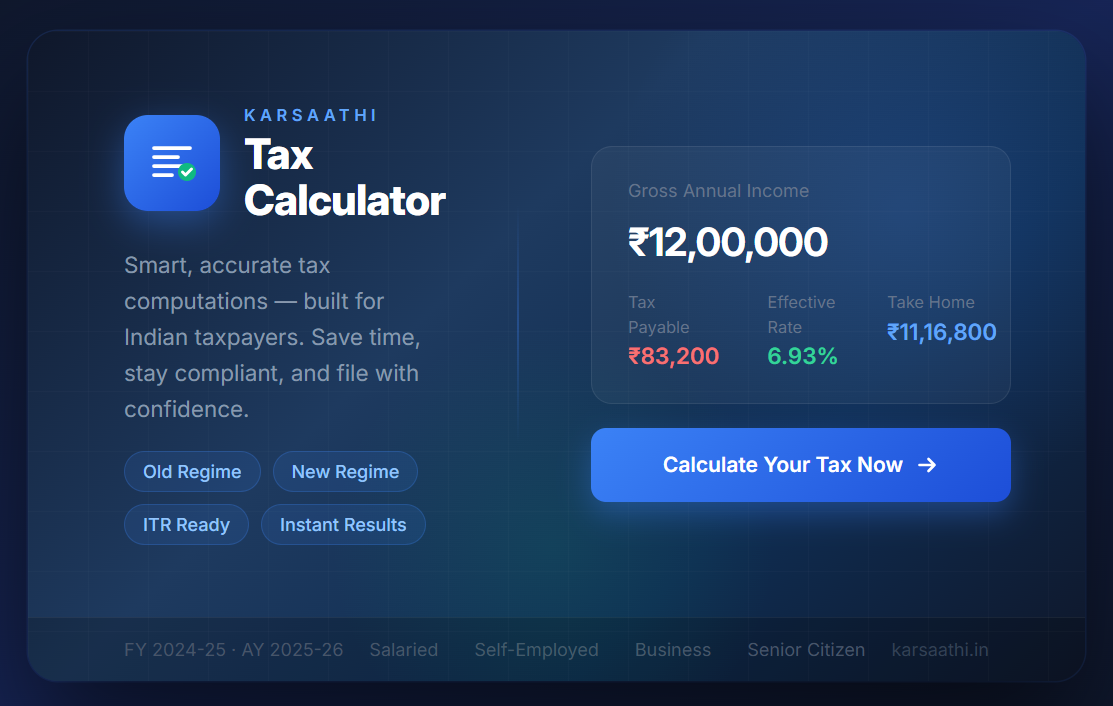

Karsaathi Income Tax Calculator

26 May, 2026 | 06:04 AM

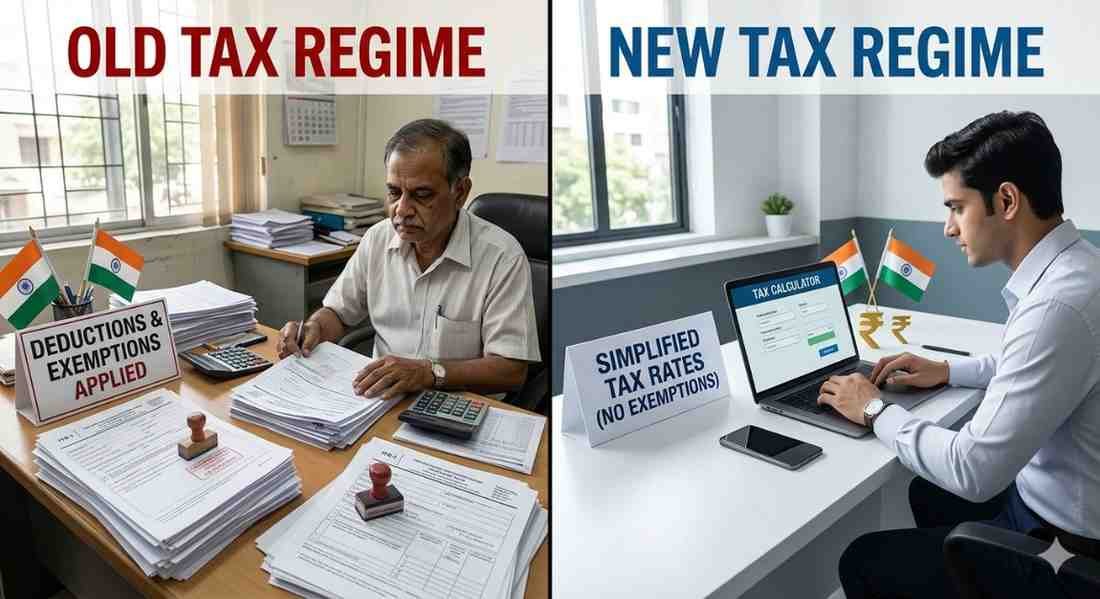

New vs Old Tax Regime Calculator

06 February, 2026 | 07:28 AM

Decoding Union Budget 2026

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

08 May, 2025 | 01:09 AM

Simple Guide to Filing ITR1 Sahaj

30 April, 2025 | 05:51 AM

Mortgage Rates Today

Popular Blogs

14 February, 2024 | 11:43 PM

Top 15 ITR Filing Documents

21 March, 2024 | 12:29 AM

The Road to Financial Freedom: Leveraging Tax Services for Long-Term Success

13 May, 2025 | 07:42 AM

Top 5 Tips for Filing ITR 4 Easily

27 February, 2024 | 11:20 PM

Why Filing ITR with No Income is Smart

14 February, 2024 | 11:39 PM

21 Ways to Save Tax From Salary

10 October, 2024 | 10:15 PM